Recording

Governing the Deal: Board Oversight Across the M&A Lifecycle

Boards play a pivotal role in shaping transaction strategy and outcomes, but effective oversight looks very different from management execution.

The Role of the Internal Auditor: Assessing and Responding to Fraud Risk

Fraud risk is persistent and evolving, driven by economic, regulatory, technological, and geopolitical pressures.

Internal auditors play a key assurance role in helping organizations assess, manage, and respond to fraud risk and deter fraud by evaluating governance, fraud risk management processes, and internal controls.

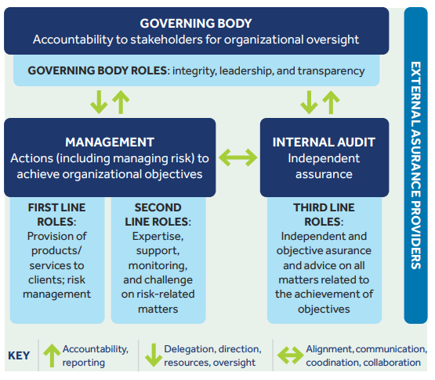

Three Lines Model*

*Refer to The IIA’s Three Lines Model – An Update of the Three Lines of Defense