Current Business Issues and Risk Considerations

Reminders About Macroeconomic Conditions

- Recession risk

- Rising interest rates

- Continuing inflation

- Tightened labor market

- Credit contraction

- Climate risk

- Uncertainty in the real estate sector (residential and commercial)

- Fluctuations in foreign currency exposure (geopolitical environment and supply chain challenges)

- Cybersecurity

- Pace of technological innovation

- Uncertain regulatory environment in the U.S and globally

Financial Reporting Considerations

- Risk assessment

- Design and operation of internal controls

- SEC Disclosures

Accounting & Reporting Considerations During Economic Uncertainty

Accounting Considerations - Evolving situations that require continual assessment and analysis, particularly whether a downward measurement adjustment is required for assets or whether new liabilities may need to be recognized.

Importance of Disclosures - Transparency for investors through evaluation of the completeness and transparency of accounting, judgments, and as well subsequent events, risks and uncertainties, and going concern assessments.

SEC Reporting Requirements – Changing economic environment often creates new and evolving risks, uncertainties, impacts, and challenges that can affect SEC registrants’ disclosures.

Internal Controls Over Financial Reporting – Whether there may be a need to design and implement new or modify existing controls to address complexities and risks associated with events that cause economic uncertainty.

Auditing Considerations – Whether there may be heightened and new risks of material misstatement or more difficulty in an auditor’s ability to obtain sufficient appropriate audit evidence for both the audit committee and management to factor into their oversight and execution of financial reporting.

Corporate Governance - Highlights the importance of boards and audit committees working closely with management, auditors, and advisors to evaluate risks and form meaningful responses to and communications about those risks. This includes the effects on employees, customers, and supply chains, including how executives are planning for contingencies.

View the publication here.

CAQ: Institutional Investor Perception of Fraud

Key Findings:

- Eight in ten investors believe fraud at U.S. public companies is medium-to-high, translating to an average of 3% of annual revenues based on investor estimates.

- Investors believe that internal audit teams hold the primary responsibility for preventing and detecting fraud, followed closely by company management and boards of directors.

- When financial fraud does occur, the plurality of investors view a company’s senior management as most responsible for the incident.

- Most investors believe that fraud prevention and detection can be more successful by placing a greater focus on monitoring transactions, especially with AI, and via employee training & culture.

- Investors believe the types of fraud most likely to occur are external, including cyberfraud, customer payment fraud, or fraud by vendors and sellers.

- Investors believe that cyberfraud has the potential to be the most catastrophic.

Fair

Safe

Autonomy

Supported

Cared For

Heard

Empowered

The Impact of Fraud at U.S. Public Companies Benchmarking Report

Association of Certified Fraud Examiners & Anti-Fraud Collaboration

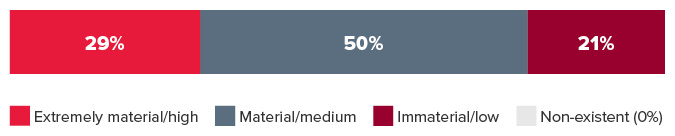

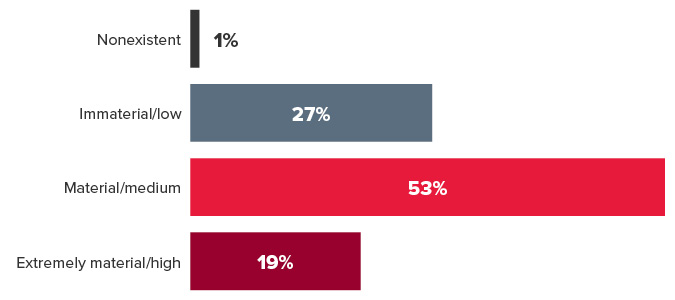

Current Overall Level of Fraud at U.S. Public Companies

- Over 70% of respondents rated the current level of fraud at U.S. public companies as medium or high.

Factors that Contribute to the Current Level of Fraud:

- Employees identified the regulatory environment as the most significant factor contributing to fraud.

- Governance respondents (board and audit committee members) pointed to the quality of external audits as most significant.

- External respondents (regulators, consultants, external auditors) considered economic conditions/environment as the top factor.

- Economic conditions/environment was the only factor ranked in the top five by all respondent groups.