2016 BDO Global Energy Middle Market Monitor

Contents

- Introduction

- Revenue Drop Hits North America Hardest

- Profits Dip to Five-Year Lows

- Investor Returns Plummet

- Funding Harder to Source; Debt Ratios Still Grow

- Exploration Stalls

- Production—and Associated Costs—Creep Up

- North American Reserves Decline, but Have Not Bottomed Out

- Data Break: What’s Going on with the Supermajors?

- What’s Next for the Industry?

- About This Study

The 2016 BDO Global Energy Middle Market Monitor reviews and analyses financial data reported by 304 publicly traded middle market oil and gas companies from 37 country and international stock exchanges from 2010 to 2015. The companies analysed reported revenues up to $1.5 billion, with median revenue of $67.6 million. Companies were primarily traded on exchanges in Australia, Canada, the United Kingdom and the United States. All data was sourced through S&P Capital IQ.

See methodology note toward the end of this report for more information.

“The middle market has been instrumental to the growth of the international energy sector, helping to decentralise the industry and spread the wealth well beyond OPEC to all corners of the globe. But the rapid growth we saw over the past decade was unlikely to last, and it appears that many may have lost sight of the energy industry’s susceptibility to boom and bust cycles. But now that the oil price downturn has checked our collective hubris, we are in a position to reorient, re-evaluate and rebuild.”

- Charles Dewhurst, Global Leader of the Natural Resources practice at BDO

Introduction

It has been two years since oil prices began their precipitous fall in mid-2014, ending the energy sector’s most recent boom and kicking off a protracted bust. With prices declining as much as 70 percent since June 2014, many of the middle market independent producers that entered the game at its height are now facing significant losses and a very real threat to their longevity in a down market. Prices have begun to rebound, reaching the $50 per barrel mark in June 2016, but we still have a long way to go before the energy industry achieves healthy growth once again.

In the 2016 edition of the BDO Global Energy Middle Market Monitor, we explore what these losses mean in terms of revenue declines, wavering investor confidence and the ability to compete with the leading industry players. Our top takeaway? No one has been immune to the price slump, and companies may be forced to make difficult choices in order to survive—but those who are able to make smart cuts and seek out creative financing opportunities are best poised to thrive when the market finally turns around.

Revenue Drop Hits North America Hardest

Year-over-year changes in median annual revenue highlight that the pain of the price slump truly hit the global energy sector in 2015: The median revenue across all companies assessed fell by about 30 percent, from $96.9 million USD in 2014 to $67.6 million in 2015.

The United States and Canada saw the most dramatic slashes to their revenues over the past year, with Canadian-listed companies’ and U.S.-listed companies’ median revenue declining by 41 percent and 44 percent, respectively. Meanwhile, Australian median revenue more or less remained stable from 2014 levels, and U.K. median revenue decreased by just 4 percent. The size of the industry in each region appears to have influenced the relative magnitude of the shifts in each country—according to the U.S. Energy Information Administration, the United States and Canada combined produced about 18 million barrels of oil equivalent per day (BPD) in 2014, compared to 906,000 BPD in the U.K. and 473,000 BPD in Australia. In other words, those countries with the most sizable oil and gas sectors were likely to feel more impact.

“Canada’s economy has been struggling for more than a year now, teetering on the brink of a full-blown recession—much of which is attributable to oil prices’ impact on the Canadian natural resources sector. In fact, recent projections have suggested that the oil production cuts forced by the Fort McMurray wildfire in Alberta are significant enough to wipe out the potential for any national economic growth in Q2 2016.”

- Michael Madsen, National Leader of BDO Canada’s Natural Resources practice

Profits Dip to Five-Year Lows

As revenues have slipped, so have profits for middle market oil and gas companies. Globally, median pretax income declined from $5.9 million in 2014 to a net loss of $30.2 million in 2015, an overwhelming 614 percent decrease. After taxes, net income dropped from $5.1 million to a loss of $30.5 million, a sevenfold decline. This data broadly reflects the volume of impairments energy companies were expected to incur as the gains of the 2010 to 2014 period eroded.

On a country-by-country basis, Canada and Australia saw the largest proportional drops in median pretax income (seeing declines of 22 times and 27 times their 2014 levels, respectively), while the U.K. and Canada saw the most significant decreases in median net income (recording declines of 19 times and 13 times 2014 levels, respectively). U.S.-listed companies posted the most substantial losses in terms of raw dollar amounts, with median pretax income declining by $175.1 million year over year and median net income decreasing $133.2 million. However, these losses amounted to an approximately 400 percent decrease from 2014—the smallest proportion seen in this year’s study.

With companies throughout the study consistently posting losses in 2015, we found that the median effective tax rate both globally and regionally came to 0 percent, reinforcing the broad economic pain caused by the price rout: Individual companies are struggling, the industry is reeling and governments worldwide are losing out on a key source of tax revenue.

Investor Returns Plummet

With revenues and profits tumbling over the past year, investors have begun to sour on middle market oil and gas companies globally. The median market cap across all companies studied dropped to $91 million in 2015 from $219 million in 2014, a 58 percent decline. Canadian-listed companies experienced the most painful contraction, with the median market cap falling by 76 percent, while the other primary countries studied posted declines more in line with the overall median.

Unsurprisingly, historic price-earnings (PE) ratios took a hit, as well. Last year, our study found that strong performance through the first half of 2014 helped cushion PE ratios from falling as sharply as oil prices did in the back half of the year. However, with no such buffer in 2015, PE ratios decreased abruptly as earnings—and investors’ expectations about performance—faltered. The median historic PE ratio fell to 6.4 this year, down from 12.4 last year and from the overall high of 25.6 in 2010.

Australia saw the most dramatic decline in median PE ratio from 2014 to 2015—69 percent—while the U.K. saw the median PE ratio drop by just 28 percent. U.S.-listed companies tracked fairly close to the overall median, with their median PE ratio declining by about 53 percent.

“The highest average oil price in the last five years occurred in 2013, and for the same period, U.K. AIM-listed oil and gas companies enjoyed their highest market capitalisations. However, the decline in oil prices over the last 15 months has had a more dramatic effect on these companies’ market capitalisations than perhaps would or should have been evident, with the average market cap falling at nearly twice the rate of oil prices in the U.K. In our view, this reflects not only the impact of the oil price environment on the sector, but also a loss of investor confidence and lack of desire to invest in what is perceived as a volatile industry.”

- Ryan Ferguson, Partner and Oil & Gas Sector Lead with BDO United Kingdom’s Natural Resources practice

Funding Harder to Source; Debt Ratios Still Grow

As margins and investor confidence have slipped, oil and gas companies have been struggling to secure capital to keep their businesses afloat. Last year’s Global Energy Middle Market Monitor found that companies had grown more leveraged as they turned to debt financing to weather the storm, and this year’s study reveals that this trend largely continued in 2015. The median debt ratio grew by nearly 25 percent this year, with Australia seeing the largest jump: The median debt ratio for Australian-listed companies doubled this year. Meanwhile, the U.K. saw a modest 11 percent increase, while Canada and the U.S. saw median debt ratios largely in line with global trends.

That said, we may expect to see this rate of growth decrease in the year to come. Throughout 2015, many banks were reticent to close the debt financing spigot, hoping to see the industry stabilise and turn around by the end of the year. Now that we’re halfway through 2016, however, we’re beginning to see more banks re-evaluate their loans to energy companies—particularly as bankruptcies proliferate.

Exploration Stalls

As prices have continued to plummet, numerous upstream oil and gas companies have put the brakes on additional exploration. According to Baker Hughes’ international rig count for May 2016, the total number of rigs in operation declined by 203 from May 2015 levels—and this decline is reflected in companies’ expenditures on exploration.

Overall, median exploration cost has decreased significantly, from $36.2 million in 2014 to just $7.9 million in 2015, a 78 percent year-over-year decline. Canada saw the largest proportional drop in median exploration cost (89 percent), while the U.S. saw the smallest (just 8 percent). Meanwhile, Australia actually saw median exploration cost increase by about 8 percent.

In addition, it becomes clear how aggressive these exploration cuts have been when we examine exploration costs’ median share of overall revenue. Globally, the median exploration cost as a percentage of revenue declined by about half—far outpacing the 30 percent decline in median revenue discussed earlier. In the United States, Canada and the U.K., median exploration cost as a proportion of revenue declined to less than 10 percent, with Canada seeing the most dramatic drop—from 27 percent in 2014 to 3 percent in 2015.

Australia, on the other hand, saw no year-over-year change in median exploration cost as a percentage of revenue, reflecting the relative stability seen in revenue in that market—again, likely a result of the modest size of the industry in its region.

“Australia’s oil and gas sector is roughly six months behind that of the United States or Canada. As a result, industry observers here are of the mind that, although we’re seeing relative stability and even modest growth right now, companies can expect to see the industry slow in the months to come. We’re actually seeing quite a bit of hedging activity as companies seek to lock in their wins and guard against the inevitable downturn ahead.”

- Sherif Andrawes, National Leader of the Natural Resources practice at BDO Australia

Production—and Associated Costs—Creep Up

While mid-market oil and gas companies were quick to cut exploration, they were much slower to curtail production; we’ve even seen, to some extent, growth in production in select markets.

With the exception of Canada, median absolute production cost grew across all primary markets analysed in this study between 2014 and 2015. U.S.-listed companies saw the slowest rate of growth, with median production cost growing by 21 percent, while the U.K. saw the fastest rate of growth, with the median cost nearly doubling. Meanwhile, Canada saw its median production cost decrease by about 12 percent. As a result of these disparate trends, the global median remained fairly stable, decreasing a modest 4 percent.

Production Costs Taper Amid Continued Market Volatility

This report was originally compiled in May 2016, using data generated by S&P Capital IQ at the end of April. Counterintuitively, this data found that production costs had continued to grow in 2015. But, in a demonstration of how rapidly the energy sector can evolve, a repeat query on S&P Capital IQ in June 2016 found that, less than two months later, production costs had declined significantly in most markets between 2014 and 2015:

| Change in Total Production Costs | Change in Median Production Cost | |

|---|---|---|

| Australia | +16% | +35% |

| Canada | -20% | -33.5% |

| U.K. | -11.5% | -6% |

| U.S. | -5% | +15% |

What lies behind this shift? A number of companies in the original dataset declared bankruptcy over the past quarter, removing their metrics from the S&P Capital IQ database. In addition, the new dataset incorporates information from late filers—some of whom are some of the most financially-strapped companies in the sample pool, and are more likely to have pursued aggressive cost-cutting than their healthier counterparts. It is clear, then, that the raw numbers only tell part of the story; who reports the information (and when they do so) can provide equally valuable information to industry observers and investors alike.

Reviewing the larger picture and the universe of information available to us, it is clear that, even with oil prices breaking the $50/barrel mark in recent weeks, the energy industry’s pain is far from over. We expect to see E&P expenditures continue to contract for much of 2016, and potentially into 2017 if prices are unable to maintain their upward trajectory.

With production costs generally growing as revenues have declined, it should come as little surprise that median production cost as a percentage of revenue has grown. Globally, production costs accounted for about 36 percent of revenue in 2015, up from 25 percent last year. U.S.- and Canadian-listed companies saw the largest increase, with both countries seeing median production cost as a proportion of revenue grow by about 13 percentage points year over year. At the same time, the U.K. and Australia saw increases of 3 percentage points and 9 percentage points, respectively.

Why are production costs on the rise despite growing pressure for companies to cut back? Though our data on this front is limited—only the United States’ and Canada’s reporting requirements generate a significant amount of data on daily production—it appears that, quite simply, companies have been reticent to halt production on projects in which they had invested heavily prior to the price crash. In addition, cash is king, with many companies continuing production in an effort to maintain some degree of cash flow. However, despite demand lagging in European and Asian markets, there is some glimmer of hope that demand is bouncing back in the United States and Canada as a variety of industries—manufacturing, chemicals, consumer businesses, etc.—take advantage of low downstream energy prices. As a result, we’ve seen median daily oil production grow by 14 percent in Canada over the past year, and 25 percent in the United States.

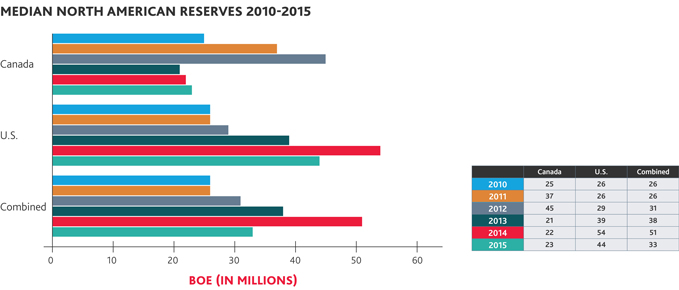

North American Reserves Decline, but Have Not Bottomed Out

Despite facing daunting industry inertia, North American companies continue to maintain robust reserves vitality. 1 Median reserves, in general, have fallen a substantial 35 percent over the past year—from 51 million barrels of oil equivalent (BOE) to 33 million BOE—but the median reserve replacement rate remains at 101 percent. While less than last year’s median replacement rate, which reached slightly more than 250 percent, this still demonstrates that middle market North American companies have been able to maintain some momentum since prices first began to fall. U.S.-listed companies posted a median reserve replacement rate of 124 percent in 2015, while Canadian-listed companies saw a median rate of 95 percent.

.jpg "2016-Global-Energy-MMM-brochure-chart-13-x679-(1).jpg")

Consistent with the findings from last year’s study, however, the rapid depletion of the unconventional assets common in North America continues to drive heated competition for new reserves. The median reserve life in Canada dropped to 8.2 years in 2015 from 10.9 years in 2014, and the median in the United States dropped from 13.7 years to 9.5 years over the same time period. The median North American reserve life, then, decreased by 4.0 years—from 13.0 years in 2014 to 9.0 years in 2015.

We continue to see North American companies seek to add to their reserves. However, with cash flow dwindling and overall resources (labour, oilfield services, etc.) contracting, the rate of reserve additions has dropped sharply. The median reserve addition in 2015, including purchases, was 28 million BOE, down 94 percent from 2014. U.S. additions decreased by about 93 percent, while Canadian additions decreased by 64 percent.

Data Break: What’s Going on with the Supermajors?

As part of our analysis for the 2016 Global Energy Middle Market Monitor, we separately evaluated five of the largest global E&P companies—ConocoPhillips, Chesapeake Energy, Devon Energy, CNOOC, and Oil and Natural Gas Corp.—to compare their performance to that of the middle market.

We found that these companies largely experienced the same pain as the middle market as supply grew, demand dwindled and prices plunged. Moreover, the sheer size of these companies amplified the scale of the losses they experienced—indeed, we’re seeing the credit agencies begin to downgrade these companies’ credit ratings, indicating that no one in the industry is immune to the effects of the downturn. But size is also working to the supermajors’ favour; despite significant setbacks, they are still well-positioned to smartly allocate resources, seek out acquisitions and make necessary cuts to rebound quickly as prices creep back up.

Key findings include:

-

Revenue: Median revenue for these companies reached a high of $29.9 billion in 2013, but dropped to $25.7 billion by 2015. Nevertheless, the median 2015 revenue still exceeded that of 2010 ($22.9 billion) by about 13 percent. Interestingly, among the middle market, median revenue in 2015 was nearly 50 percent higher than median revenue in 2010—suggesting that the middle market saw greater overall gain from the oil boom of the last half‑decade.

-

Income: The median 2015 pretax income for these companies amounted to a $7.2 billion loss, and after taxes, they posted a median loss of $4.4 billion. These losses were, on a proportional basis, far more significant than those seen among the middle market.

-

Profitability: The median market cap decreased by 32 percent, from $46.2 billion in 2014 to $31.2 billion in 2015. Meanwhile, the median PE ratio declined by 25 percent. Both of these declines are smaller than that of the middle market.

-

Debt: From 2014 to 2015, the median debt ratio among the five supermajors analysed grew by nearly 25 percent, consistent with the growth seen among the middle market. However, overall, these larger companies are less leveraged than their mid-market counterparts, with the median debt ratio generally being 3 to 5 percentage points less than the middle market between 2010 and 2015.

-

Exploration: The median exploration cost declined from $1.7 billion to $1.5 billion between 2014 and 2015. However, median exploration cost in 2015 remained significantly higher—about 45 percent—than 2010 levels. As a percentage of revenue, the median exploration cost increased by about 50 percent, but the total share of revenue exploration costs occupied remained fairly small, with the median totalling about 6 percent. Since median exploration cost as a percentage of revenue declined for the middle market companies analysed, it seems likely that the supermajors simply did not cut their exploration activities quite so aggressively.

-

Production: Like the middle market, between 2014 and 2015, median daily oil production and median production cost as a percentage of revenue grew, while median absolute production cost decreased. Median daily oil production grew by 10 percent, and median production cost as a proportion of revenue increased by 6 percentage points—both smaller increases than what we’ve observed among the middle market. The absolute decline in median production cost, however, totalled about 11 percent, a fairly significant departure from the 4 percent overall decrease seen among mid-market companies.

-

Reserves and Reserve Additions: When it comes to reserves vitality, it is no surprise that total reserves and reserve additions among the supermajors outpace that of the middle market. Median reserves for the supermajors remained roughly flat between 2014 and 2015 at about 3.7 billion BOE, and median reserve additions (including purchases) totalled about 266 million BOE in 2015. Additions decreased by about 50 percent from 2014 to 2015, but the decline remains substantially less than the 94 percent decrease seen among North American mid‑market companies.

-

Reserve Life and Replacement: Despite their advantage in terms of volume, the supermajors analysed fell behind the middle market when it came to reserve replacement. Whereas the median reserve replacement ratio for mid-market North American companies was about 101 percent in 2015, the supermajors achieved a rate of just 57 percent. In fact, over the 2010-2015 period, we saw the middle market consistently outpace the supermajors on this front. In terms of reserve life, the supermajors achieved parity with the middle market, with the median reserve life in 2015 equalling about 9.0 years.

What’s Next for the Industry?

The 2016 Global Energy Middle Market Monitor paints a bleak near-term picture for oil and gas companies, both supermajor and mid-market alike. Supply and demand remain in disequilibrium, the number of companies facing bankruptcy continues to grow, and access to capital and credit has begun to dry up. Though oil prices have crept back up from the painful lows of January 2016, they have yet to achieve a level that could facilitate sustained growth, and it is unclear when the industry may once again enjoy $90-$100 per barrel prices, if ever.

So, what can middle market oil and gas companies do to weather the storm now and prepare for a more stable future? While it will ultimately vary by market and circumstance, companies have a number of options at their disposal:

Seek opportunities to diversify the business

Those companies that have the resources to explore different facets of the industry—whether that means opportunities in natural gas production and exportation, midstream infrastructure, oilfield services or completely different segments of the natural resources space—should consider doing so. Part of what allowed some of the larger companies to stave off the worst of the downturn for as long as they did was their ability to derive revenues from other segments of their businesses.

Consider alternative funding sources

Though debt financing may be drying up for many companies, other capital providers remain interested. Going private may be one option; private equity buyers have been eyeing the oil and gas industry since the start of the price slump, carefully watching valuation trends and seeking out companies with the potential to survive the downturn and emerge profitable when prices rebound. In some countries, government funding might be an option; the Canadian government, for example, does provide some level of grant money to help support the oil and gas sector.

Evaluate hedging arrangements

In 2014 and early 2015, many companies benefitted from the hedging contracts they had locked in while oil prices were still high. Though those contracts eventually expired and could no longer protect companies from the price crash, companies should closely monitor oil prices and consider entering into hedging contracts when prices once again reach sustainable, profitable levels.

Slim down

Many companies have already begun the painful process of making cuts across their businesses, from selling non-core assets to implementing layoffs. The key, however, is to be as strategic as possible when making these cuts. No company wants to be left behind when the industry turns around, scrambling for skilled labour, access to pipeline and refining infrastructure, or customers.

Continue to prioritize innovation

Though innovation may require significant upfront costs, it can result in major cost reductions or production improvements down the line. Innovation undertaken by nimble, less risk-averse middle market E&P companies drove much of the industry’s growth prior to the price crash, and may be what helps to turn the sector around. Companies should explore their options for financing or offsetting the costs of innovative research, such as tax incentives for research and development activities or government grants/contracts.

Explore restructuring options

While bankruptcy and restructuring regimes vary by country, these may be a viable option of last resort to help distressed companies settle their debts and turn around their businesses. While such arrangements may generate significant near-term pain, they may help position struggling businesses to grow in a more favourable economy.

About This Study

The 2016 BDO Global Energy Middle Market Monitor reviews and analyses financial data reported by 304 publicly traded middle market oil and gas companies from 37 country and international stock exchanges from 2010 to 2015. Eighty-one percent of the companies reviewed were listed on exchanges in Australia, Canada, the United Kingdom and the United States. Additional country exchanges represented include Argentina, Belgium, Brazil, Bulgaria, Denmark, Finland, France, Germany, Hong Kong, India, Indonesia, Israel, Kazakhstan, Malaysia, the Netherlands, New Zealand, Norway, Pakistan, the Philippines, Poland, Portugal, Romania, Russia, Serbia, Singapore, Sweden, Trinidad and Tobago, Turkey and Vietnam.

The companies analysed reported revenues up to $1.5 billion, with median revenue of $67.6 million.

Data was gathered from S&P Capital IQ. All monetary data was converted to U.S dollars.

Due to differences in public company reporting requirements, reserves vitality data (total proved reserves, reserve additions, reserve replacement ratio and reserve life ratio) and daily production data were only available for U.S.- and Canadian‑listed companies.

SHARE