2026 Shareholder Meeting Agenda: How Can Directors Better Prepare?

As corporations prepare for their 2026 annual shareholder meetings, BDO invites you to explore important findings from our 2026 Shareholder Meeting Agenda publication.

Achieving Effective Internal Control Over GenAI

This report provides a COSO-aligned way to govern GenAI responsibly by adapting COSO’s 2013 Internal Control–Integrated Framework (five components, 17 principles) into GenAI-specific practices rather than creating a new framework.

COSO Internal Control Integrated Framework Components

Board Takeaways: Governing for Persistent Volatility

Geopolitics and Growth – Strategic Foresight in a Volatile World

| Board Takeaway | Board Action |

| Elevate Geopolitical Risk | Embed geopolitical, trade, and tariff risk as a standing priority in Board and Audit Committee agendas, explicitly linked to strategy and performance. |

| Pressure-Test Assumptions | Require scenario analyses that stress earnings, liquidity, supply chains, and capital access across multiple geopolitical and trade outcomes. |

| Strengthen Reporting & Controls | Confirm that financial reporting, disclosures, and ICFR reflect tariff impacts, economic uncertainty, and heightened fraud risk. |

| Anticipate Shareholder/ Stakeholder Scrutiny | Align with management on a clear, consistent investor narrative covering risk exposure, mitigation strategies, and contingency planning. |

| Increase Engagement Cadence | Assess whether more frequent briefings, special sessions, or external expertise are needed as global conditions evolve. |

CAQ Annual Institutional Investor Survey

The Center for Audit Quality and KRC Research surveyed 300 U.S. institutional investors to examine how investors perceive the audit’s role amid changing expectations around assurance, innovation, and oversight, highlighting investor priorities and the themes influencing confidence and trust in capital markets.

How often do you use each of the following types of company disclosures to make investment decisions?

How much would you trust the accuracy of disclosures if it were audited by an independent public company audit firm?

CSRD: Final Omnibus Updates

Key Revisions:

- Value‑chain cap: SME ≤1,000 employees limited to voluntary standards.

- European Sustainability Reporting Standards (ESRS) simplification: ~70% fewer data points; streamlined materiality.

- Assurance: Limited assurance only; EU standard expected July 2027.

- Exemptions: Financial Holding Companies

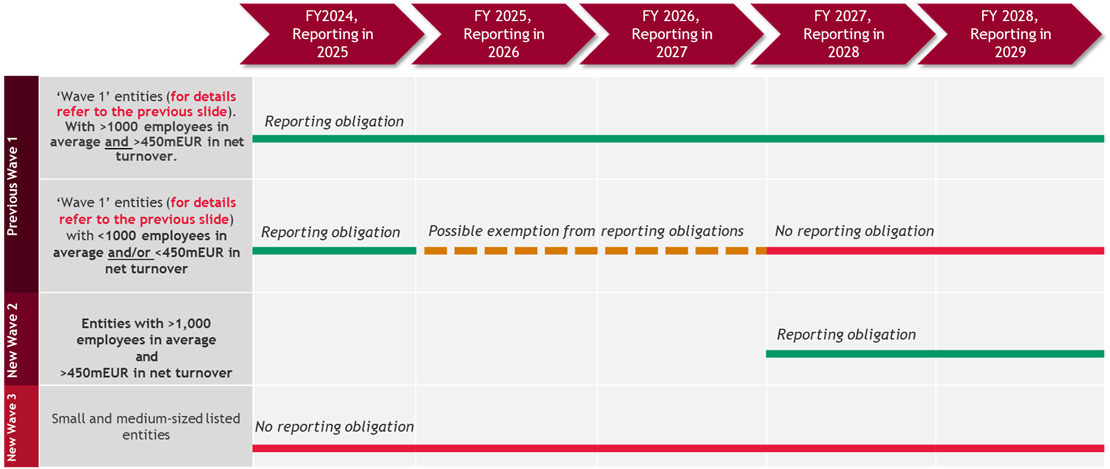

| Compliance Wave | Initial Scope | Reports Due (Under Omnibus) | Omnibus Revision (Dec 2025) |

| Wave 1 | Large Listed Entities:

| 2025 (FY24 Data) | Large Entities: US companies that have >1,000 employees and revenue >€450M during the financial year, including

|

| Wave 2 | Other Large Entities: Two of the following:

| 2028 (FY27 Data) | |

| Wave 3 | Listed SMEs, small credit institutions and insurance undertakings | Wave 3 entities removed from scope | |

| Wave 4 | Non-EU Groups:

| 2029 (FY28 Data) | Consolidated Groups: US companies that

|

Revised CSRD: Reduced Scope for EU Companies

Omnibus: Agreed Position and What is Changing from ‘Wave 1’ Entities Position

Revised CSRD: Reduced Scope for Non-EU Companies

Which Entities are in Scope?

- Non-EU groups that:

- Generate EU net turnover; and

- Have ≥ one EU subsidiary or branch.

- Financial holding company exemption applies.

Scope Thresholds for Non-EU Parent Groups

- EU net turnover ≥ 450m EUR in each of the last two consecutive financial years; and

- EU subsidiary/branch net turnover ≥ 200m EUR in the previous financial year.

Other Key Requirements

- EU subsidiary/branch shall publish and make available a group-level sustainability report (prepared by the non-EU parent)

- Timing: First reporting for FY 2028 (published in 2029).

- Standards:

- Sustainability reporting standards for third- country companies (expected 2027)

- Option to report in accordance with ESRS

Climate-Related Disclosures: California SB 261 and SB 253*

| SB 261: Climate-Related Financial Risk Disclosure | SB 253: Climate Corporate Data Accountability Act | |

| Applicability | Companies >$500M in global revenues are required to disclose biennially climate related-risks and adaption measures | Companies >$1 billion in global revenues are required to disclose and obtain assurance over annual Scope 1, 2 and 3 greenhouse gas (GHG) emissions data |

| Scope | Does business in CA | Does business in CA |

| Type of Entity | Public & Private | Public & Private |

| Timelines | Reporting of climate-related risks delayed pending resolution of hearing held by the Ninth Circuit Court on January 9th, 2026. | 2026: Disclosure of Scope 1 & 2 (2025 Data) ^ 2027: Disclosure of Scope 3 (2026 Data) |

| Assurance | None | Limited assurance on Scope 1 and 2 emissions (from 2027) ^^ Reasonable assurance on Scope 1 and 2 emissions (2030) Limited assurance on Scope 3 emissions (2030) |

| Penalties for non-compliance* | Up to $50,000 per reporting year | Up to $500,000 per reporting year |

| Additional relevant updates | Refer to timelines above. | ^ Only for 2026 and for those companies that were not collecting Scope 1 and 2 emissions when the Enforcement Notice was issued in December 2024. Such entities should submit a non-reporting statement to CARB’s public docket. ^^ Limited assurance is not required for 2026 submissions. |

* Companies should consult with legal counsel to determine their obligations under California’s climate disclosure laws.