Updated: Main Street Lending Program Now Open to Nonprofits

On July 17, the Federal Reserve announced release of an expansion to its Main Street Lending Program (MSLP) to address the liquidity needs of nonprofit organizations that have been impacted by the COVID-19 pandemic. The MSLP was established by the Federal Reserve earlier this year when the Treasury carved out $75 billion of the available $454 billion under Title IV of the Coronavirus Aid, Relief, and Economic Security (CARES) Act to make an equity investment in a special purpose vehicle (SPV), which enabled the flow of credit to small and medium-sized businesses that were in good financial standing prior to the COVID-19 crisis.

The new program incorporates public feedback on the proposed program that had been announced on June 15th. Previously, nonprofit organizations were not eligible to participate in the program given their absence of EBITDA, a key underwriting metric required for the three existing MSLP facilities. However, the Federal Reserve then evaluated the feasibility of adjusting the borrower eligibility criteria and loan eligibility metrics of the program for nonprofit organizations.

Under the expansion, tax-exempt organizations under section 501(c)(3) or 501(c)(19) of the Internal Revenue Code would be eligible to apply. It is also important to note that organizations that have received Paycheck Protection Program (PPP) loans and Economic Injury Disaster Loan (EIDL) program funds could also apply for a loan under the Main Street Lending Program provided they are otherwise eligible. Nonprofit borrowers participating in the MSLP may not also participate in the Primary Market Corporate Credit Facility or the Municipal Liquidity Facility

According to Federal Reserve Chair Jerome Powell, “nonprofit organizations are critical parts of our economy, employing millions of people, providing essential services to communities, and supporting innovation and the development of a highly skilled workforce. Nonprofits provide vital services across the country and we are working to help them through this difficult time.”

Loan Terms

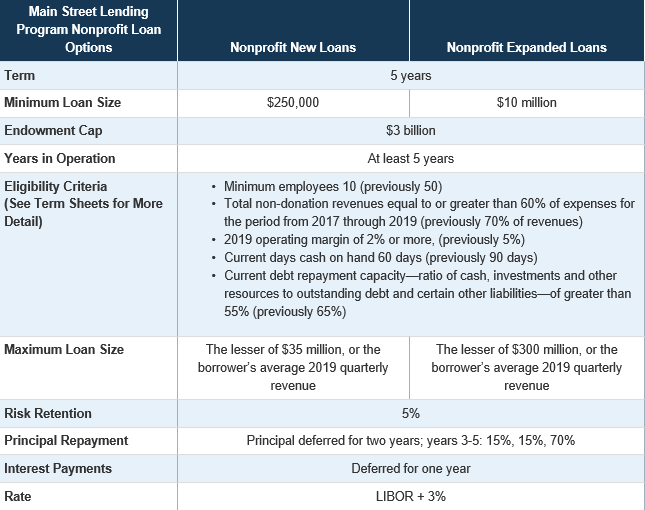

The nonprofit facilities are similar to the three MSLP facilities available to for profit small and medium-sized businesses. The loan terms such as the interest rate, deferral of principal and interest payments, and a five-year term are the same. Principal payments are fully deferred for the first two years of the loan, and interest payments are deferred for one year.

The nonprofit loans range between $250,000 and $300 million based upon an organization’s operating performance, liquidity and ability to repay debt. Two loan facilities are offered under the current program:

-

organizations entering into loans with new lenders - Nonprofit Organization New Loan Facility (NONLF)

-

organizations wishing to increase an existing loan or line of credit with an existing lender - Nonprofit Organization Expanded Loan Facility (NOELF).

Currently certain businesses are Ineligible Businesses, such ineligibility established by provisions of the Paycheck Protection Program of the CARES Act and cannot participate. The application of these restrictions to the Facility may be further modified by the Federal Reserve.

The compensation, stock repurchase, and capital distribution restrictions that apply to direct loan programs under section 4003(c)(3)(A)(ii) of the CARES Act apply here as well.

Eligible Borrowers should undertake good-faith efforts to maintain payroll and retain employees, in light of its capacities, the economic environment, its available resources, and the need for labor.

Because a nonprofit does not have some of the financial characteristics of a for-profit to measure its finances, a nonprofit borrower’s eligibility requirements have been modified from the for-profit facilities to reflect the operational and accounting practices of the nonprofit sector. The eligibility requirements are outlined below and all will have to be met for a nonprofit to be eligible for the MSLP.

-

Non-Donation revenues - Proposed limits on organizations with donation based-funding was eased from a requirement that donations be less than 30% of 2019 revenues to non-donation revenue being greater than or equal to 60% of expenses. FAQs issued July 31 (link below) provide definitions of donation revenues which allow government grants, revenues from a supporting organization, grants from private foundations that are disbursed over the course of more than one calendar year, and certain contributions of property to be excluded from the definition of donations.

-

Operating margin - Borrowers must have a ratio of adjusted 2019 earnings before interest, depreciation, and amortization (EBIDA) to unrestricted 2019 operating revenue, greater than or equal to 2%.

-

Cash on Hand - Borrowers must have a ratio (expressed as a number of days) of liquid assets at the time of loan origination to average daily expenses over the previous year, greater than or equal to 60 days.

-

“Liquid assets” are defined as unrestricted cash and investments that can be accessed and monetized within 30 days. A nonprofit organization may include in “liquid assets” the amount of cash receipts it reasonably estimates to receive within 60 days related to the provision of services, facilities, or products, or any other program service that exceed its reasonably estimated cash outflows payable within the same 60-day period.

-

Debt repayment capacity - The ratio of unrestricted cash and investments to existing outstanding and undrawn available debt, plus certain other liabilities, is greater than 55%.

The nonprofit loan program is available to organizations that have been continuously operating for at least five years with a minimum of 10 (originally proposed to be 50) and maximum of 15,000 employees, or 2019 annual revenues of $5 billion or less. Organizations with endowments exceeding $3 billion are excluded from participation. An affiliated group of entities can participate in only one Main Street facility and the maximum loan applies to the group.

The chart below summarizes key proposed terms.

.png)

Detailed descriptions of the nonprofit MSLP programs are available via term sheets by the Federal Reserve:

Nonprofit Organization Expanded Loan Facility Term Sheet (PDF)

Nonprofit Organization New Loan Facility Term Sheet (PDF)

Application Process

While lenders are currently able to register, the nonprofit Main Street loan application process is not yet open. Borrowers should carefully review the certifications and covenants in the MSLP term sheets and will need to certify as to certain restrictions on debt repayment and compensation, as well as prohibited conflicts of interest and their ability to meet their short-term financial obligations. The FAQs (above) add Appendices providing a Loan Document Checklist, borrower and lender required certifications and covenants for each facility, and tables describing the annual and quarterly financial records requirement. Application and reporting forms are obtained by the borrower from the lender. The term sheets (above) contain minimum requirements for the Program. Lenders will apply their own underwriting standards. The Main Street SPV will cease purchasing loan participations on December 31, 2020, which was extended from the original September 30 deadline.

BDO Insight

The expansion of the MSLP to nonprofits will provide additional critical liquidity to organizations affected by the current pandemic above and beyond what was provided by the PPP and EIDL program. Organizations should begin forecasting anticipated cashflow needs over an extended period. Effective forecasting will determine how a Main Street loan could help meet those needs.

Nonprofits should also analyze the term sheets for each new Main Street facility and determine the potential facility that is best aligned with their operational strategy and risk profile. In particular, they should consider the loan amount they would qualify for under each facility and whether or not they can (or would be willing to) provide any requisite collateral.

Further, interested organizations need to pay close attention to the required covenants/restrictions to make sure they can stay in compliance. Finally, existing lenders may have to approve the acceptance of additional obligations, so nonprofits should begin speaking with them about this loan option.

It is important to note that the MSLP, including the expansion to nonprofits, is continuously evolving. Monitor the Federal Reserve’s website and visit BDO’s Crisis Response Resource Center for the latest program updates and details.

Be sure to keep up with the latest happenings in the nonprofit industry by subscribing to our blog, and following us on Twitter @BDONonprofit.

SHARE