The U.S. Small Business Administration’s (SBA’s) flagship 7(a) loan program has long been a lifeline for small businesses by providing financial assistance through federal government guaranteed loans. However, the SBA does not lend the money directly. Instead, it guarantees a portion of the loan made by a participating lender, which reduces the lender’s risk and encourages it to provide funding that might otherwise be unavailable to the small business.

Until recently, the SBA 7(a) loan program had posed significant hurdles for companies pursuing employee ownership through employee stock ownership plans (ESOPs). Thanks to recent changes, the SBA 7(a) loan program is emerging as a powerful tool that can help facilitate liquidity, succession planning, and employee engagement.

The Landscape of SBA 7(a) Lending

Since its establishment in 1953, the SBA has played a vital role in fostering the growth and sustainability of small businesses across America.

Today, one of its most popular programs, the 7(a) loan program, is used as a flexible source of working capital, business acquisition funding, and real estate financing.

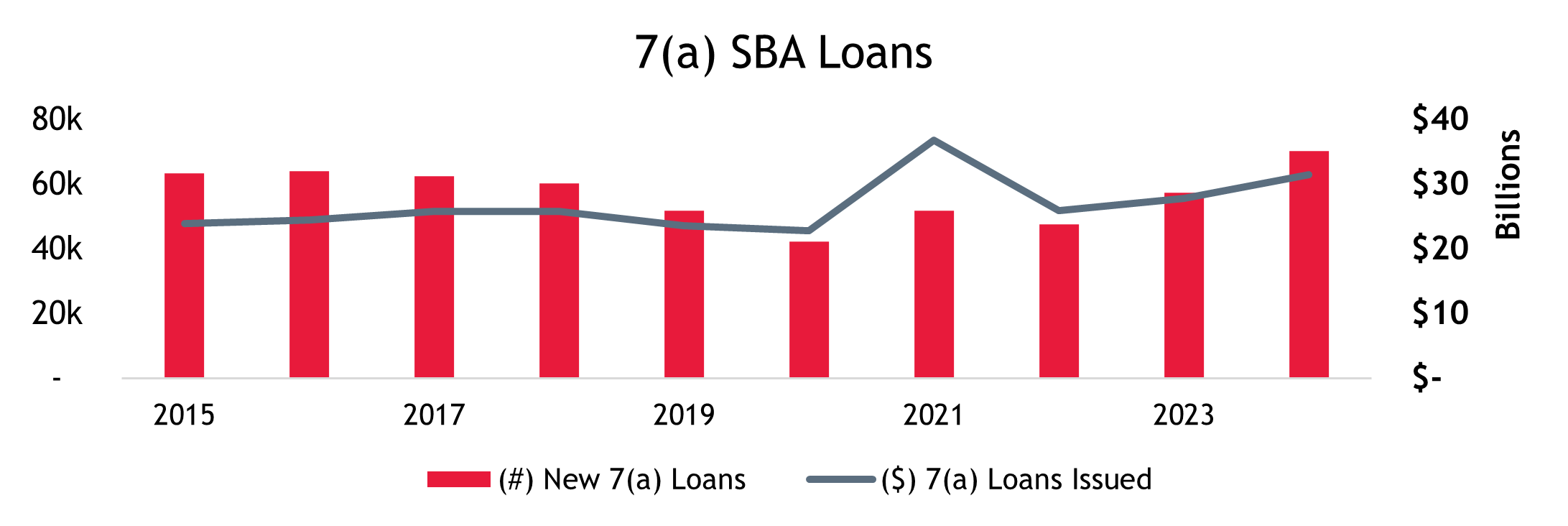

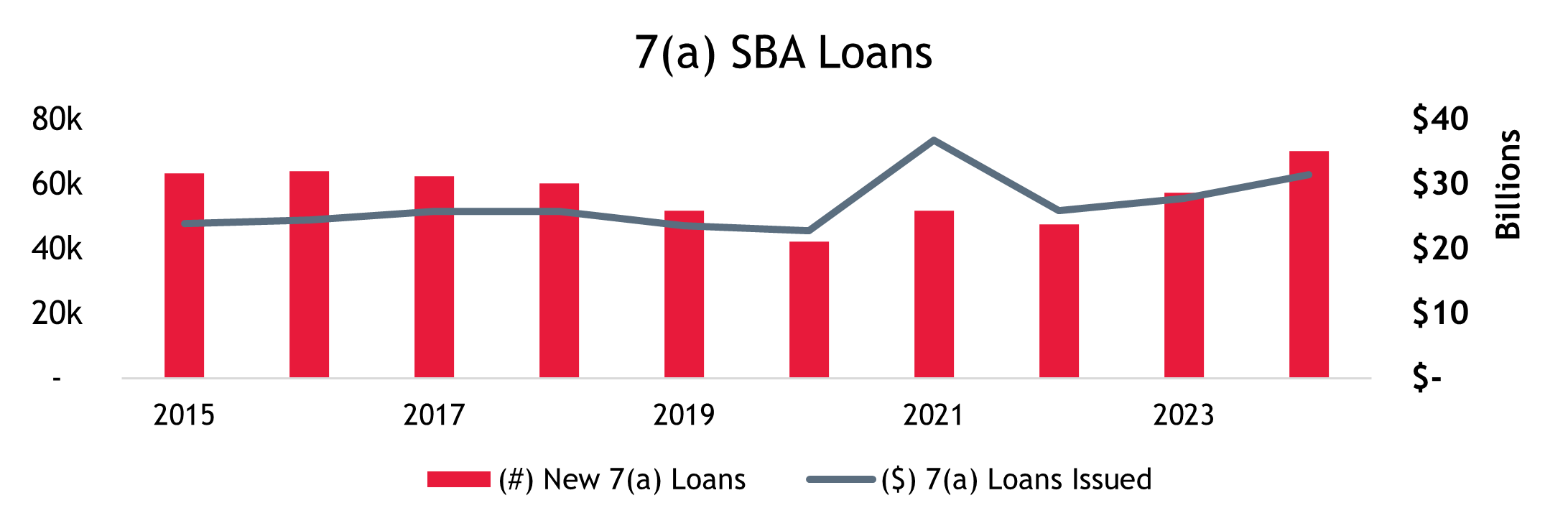

Despite the popularity and versatility of the 7(a) program (over $31 billion in new loans were issued in 2024), SBA loans historically presented challenges for certain transaction types, particularly ESOP formations.

Historical Barriers to ESOP Financing with SBA Loans

While ESOPs have long been celebrated as an effective way to encourage employee ownership and to provide an exit strategy for closely held businesses, their intersection with SBA lending faced significant hurdles for many years.

1. Equity Injection

The SBA requires a minimum 10% equity injection from a source outside the business for any change of control financed with an SBA loan. In ESOP transactions, this poses a challenge because the ESOP trust, as a tax-qualified retirement plan subject to the Employee Retirement Income Security Act of 1974 (ERISA), cannot provide the required equity. As a result, a non-ESOP shareholder must provide the capital, which can undermine the tax benefits of 100% employee ownership.

2. Personal Guarantee

To manage risk and reduce defaults, the SBA requires a personal guarantee from any shareholder who owns a 20% or greater stake in the business. However, Internal Revenue Service (IRS) and U.S. Department of Labor (DOL) ERISA rules prohibit an ESOP from guaranteeing loans. While the SBA exempts ESOPs from this requirement, it mandates that any other shareholder, even those with less than 20% ownership, provide a personal guarantee. Combined with the equity injection requirement, this effectively prevented any 100% sale to an ESOP and required ¬selling shareholders to personally guarantee the loans.

3. Approval Process

Even when companies and shareholders were willing to meet the equity and guarantee requirements, ESOP-related loans faced another hurdle: exclusion from the SBA’s Preferred Lender Program (PLP). Instead, these transactions had to be processed through the SBA’s General Processing Center, resulting in slower approvals. Because SBA specialists were less familiar with ESOPs, these loans faced increased scrutiny, longer wait times, and more documentation requests, making the process both lengthy and unpredictable.

Recent Changes: Opening the Door for ESOPs

Recognizing the potential of ESOPs to drive employee engagement and preserve local businesses, major changes over the last several years have enabled and encouraged the use of 7(a) loans for ESOP transactions.

Main Street Employee Ownership Act of 2018

This legislation expanded the SBA's authority to guarantee loans for ESOP formations and allowed guaranteed loans to cover transaction costs, provided the ESOP acquires at least 51% or more of the business. While this change helped reduce a major hurdle for companies considering ESOPs, the expenses associated with setting up the trust remain excluded.

SOP 50 10, Version 7 (2023)

SOP 50 10 7.1 streamlined ESOP loan approvals by removing the requirement for direct SBA review. It also eliminated equity injection requirements for controlling-interest ESOPs and clarified that personal guarantees are necessary only if ownership is retained outside the ESOP. Sellers who retain any ownership must personally guarantee the loan.

SBA Procedural Notice Control No. 5000-858322 (2024)

This guidance removed the requirement for a separate independent business valuation for SBA 7(a) loans involving ESOPs. Thus, the ESOP trustee’s valuation can satisfy the SBA’s stock valuation requirement, eliminating the need for a second appraisal. Previously, dual valuations increased costs, delayed transactions, and raised fiduciary concerns due to potential discrepancies.

SBA Procedural Notice Control No. 5000-865754 (2025)

Most modifications to the SBA 7(a) programs have been advantageous to ESOPs, but some of the newer requirements may increase the administrative burden for SBA lenders. In response to Executive Order 14159, which directs the SBA to identify and stop the provision of any public benefits to illegal aliens not authorized to receive them, the SBA now obligates lenders to confirm that all beneficial owners are eligible, which is especially challenging for ESOPs given their broad ownership base. Even though the majority of ESOP transactions will likely meet this requirement, the rule represents an additional obstacle that must be addressed. Collectively, however, these changes make ESOP transactions more flexible, accessible, and timely, reducing administrative barriers and making employee ownership a more attainable option for small businesses.

SBA 7(a) Loans: Key Features for ESOP Transactions

SBA 7(a) loans for ESOP purchases follow the same guidelines as other SBA business acquisition loans, with several ESOP-specific considerations:

- Loan Amounts: The standard maximum is $5 million per loan under the 7(a) program.

- Term: Up to 10 years for business acquisitions. If real estate is included, the term can extend to 25 years.

- Interest Rate: Typically variable, based on the Prime Rate plus a negotiated spread. Rates are often competitive with conventional market rates, though they may be slightly higher.

- Collateral: All available business assets are usually pledged as collateral.

- Equity Injection: Not required in the case of 100% ESOPs.

- Seller Financing: Permitted if subordinated to SBA debt and often required to be on standby for a specified period.

Is SBA Financing the Right Choice for Your ESOP?

Pros

- Longer Term: Amortization periods of up to 10 years can ease cash flow burdens compared to the shorter terms often provided in commercial loans.

- Larger Loans: The extended amortization with SBA loans may allow for more cash at closing, especially for smaller companies, than traditional bank financing.

Cons

- Fees: SBA guaranty fees typically range from 2.5% to 3.0% of the total loan value, which is higher than the 25-30 basis points (BPS) charged by many traditional lenders.

- Interest Rates: SBA loan interest rates are usually slightly higher than those in non-SBA financing, although actual rates depend on the company and prevailing benchmark rates.

- Size Limitations: The $5 million cap may limit use for larger companies or transactions. Some banks may offer a pari passu loan (where multiple lenders share equal priority rights to repayment, so they are paid back on the same level without preference) alongside the SBA loan to help address this limitation.

- Structuring Considerations: While SBA loans have become a viable option for ESOP transactions, they remain more rigid than other financing structures and may limit features commonly found in ESOP transactions, such as earnouts and warrants.

Case Study: Achieving 100% Employee Ownership with SBA Financing

A prominent architecture and interior design firm with over 30 years in business was evaluating succession options. Traditional partnership models and buy-sell agreements proved unworkable, especially as key partners exited and conventional bank financing was limited by firm size and operational constraints.

Seeking liquidity for retiring owners and a structure that preserved the firm’s legacy without excessive debt, the company pursued a 100% ESOP sale, partially financed through an SBA 7(a) loan. The transaction delivered:

- Enhanced liquidity at closing through substantial SBA-backed financing, allowing a larger portion of the sale to be funded upfront. With a 10-year amortization, the 7(a) loan was able to reduce annual debt service and support long-term ESOP sustainability.

- Continued leadership involvement, with the founders remaining as principals to provide continuity and mentorship to the next generation of employee-owners.