Key Changes Under the OBBBA

Several tax law changes introduced by the OBBBA have implications manufacturers need to incorporate into planning, including:

- Restoration of 100% Bonus Depreciation: The OBBBA permanently restores 100% bonus depreciation, which will allow taxpayers to immediately deduct the full cost of most business assets placed in service after January 19, 2025. The legislation also creates a new category of expensing for building property used in production activities. For manufacturers, this change effectively reduces the after-tax costs of capital investments in equipment or facility upgrades.

- Changes to Research Expensing: The bill permanently restores the expensing of domestic research costs, beginning in tax year 2025. For many manufacturing companies, these changes restore important capital efficiencies and could incentivize innovation.

- Restoration of More Favorable Calculation of ATI for Purposes of the Interest Deduction Limit: The bill permanently removes amortization and depreciation from the calculation of adjusted taxable income (ATI) for purposes of Section 163(j), which limits the deduction for interest expense to 30% of ATI. Since manufacturers often finance expansion plans via debt, this change allows more interest to be deducted, thereby reducing taxable income.

- Changes to Clean Energy Subsidies: The OBBBA eliminated or accelerated the phaseout of many clean energy credits, which may impact whether manufacturers pursue clean energy initiatives going forward. Solar and wind projects that qualify for the production tax credit under Section 45Y and the investment tax credit under Section 48E must begin construction before July 4, 2026, or be placed in service before December 31, 2027. There are also new sourcing rules to qualify for the credit under Section 45X for manufacturing battery, wind, solar, and other energy components.

- Increase in tax credit for eligible chipmakers: Semiconductor manufacturers may look to take advantage of the Section 48D advanced manufacturing investment credit, which increased from 25% to 35% under the new legislation. To be eligible, semiconductor manufacturers must break ground on new U.S. chip facilities before the end of 2026.

BDO’s Take

Depending on their business strategy and needs, manufacturers can use any savings realized to fund capital investments, fuel research and development spending, or just shore up balance sheets. Because manufacturers’ bottom lines have been hit especially hard this year due to tariff changes, some may eschew aggressive capital investments and instead use cost savings to preserve profitability.

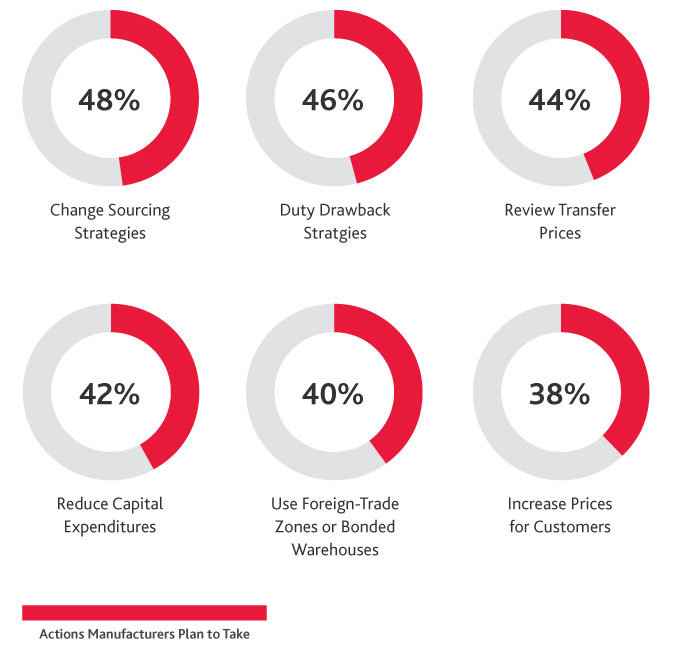

Next Steps for Navigating Trade Uncertainty

In the months ahead, manufacturers plan to deploy a variety of tactics to respond to shifting tariff policies.

Trade tensions and shifting economic alliances are motivating manufacturers to reassess their transfer pricing policies because the cost of the new tariffs has significantly decreased profit margins. As companies update their transfer pricing protocols, they must keep strong documentation and be prepared to respond to audits from global tax authorities, which 38% of survey respondents predict will be a significant challenge in the next 12 months.

Sourcing remains top of mind, with manufacturers shifting suppliers and even working with suppliers to adjust their own sourcing strategies to mitigate tariffs’ impact. Because tariffs and their effect on global supply chains remain in flux, manufacturers are making less intensive moves within their supply chain — whether by reviewing transfer prices, identifying alternative suppliers, or locking in competitive costs — rather than taking costly action to overhaul their network. However, importers are universally working with every player in their global supply chains – including vendors and customers – to “share the cost” of the new tariffs in the form of price surcharges or rebates.

Onshoring operations, for example, was a common strategy some manufacturers deployed in the past 12 months. However, because the tariff environment continues to change so quickly, manufacturers have refocused their efforts on smaller actions, such as innovative routing options, to optimize supply chain operations.

To navigate evolving policies, manufacturers should develop strategic and adaptive frameworks that can accommodate multiple tariff scenarios. To do so, elevating tax and customs leadership to C-suite conversations is key. These teams should be at the table to offer real-time intelligence on policy developments and strengthen risk management capabilities, particularly as the Department of Justice plans to increase enforcement on tariff violations.