Income Tax Accounting Hot Topics: Year End 2020

Many of the significant tax developments that were announced during 2020 may have income tax accounting considerations, including the Coronavirus Aid, Relief and Economic Security Act (CARES ACT) provisions, proposed and final Treasury regulations, and global tax relief measures related to COVID-19. BDO discusses the ASC 740 considerations of these developments and highlights some income tax accounting issues impacted by COVID-19.

Key ASC 740 Considerations

Goodwill impairment

The economic impact of COVID-19 will increase the likelihood that a company may have an impairment to goodwill. Goodwill impairments present unique accounting challenges, and several income tax accounting implications should be considered. Coordination between financial reporting and the tax department is essential in determining the pretax and tax implications of goodwill impairments.

When determining the fair value of a reporting unit, the company should determine the structure of the hypothetical disposition, whether it is a taxable or non-taxable transaction. This evaluation considers (a) which transaction results in the highest economic value to the seller, (b) the feasibility of the structure and (c) whether the structure is consistent with a market participants’ view.

The tax accounting for the impairment depends on whether the goodwill is nondeductible (“Component 2 excess book goodwill”) or deductible (“Component 1 tax goodwill”). Where there is an impairment of tax-deductible goodwill, a simultaneous equation will be required to compute the deferred tax adjustment, and this calculation will impact the amount of the impairment loss. Alternatively, if the goodwill is not tax deductible, there is no tax benefit recorded since no deferred taxes are recorded on Component 2 book over tax goodwill.

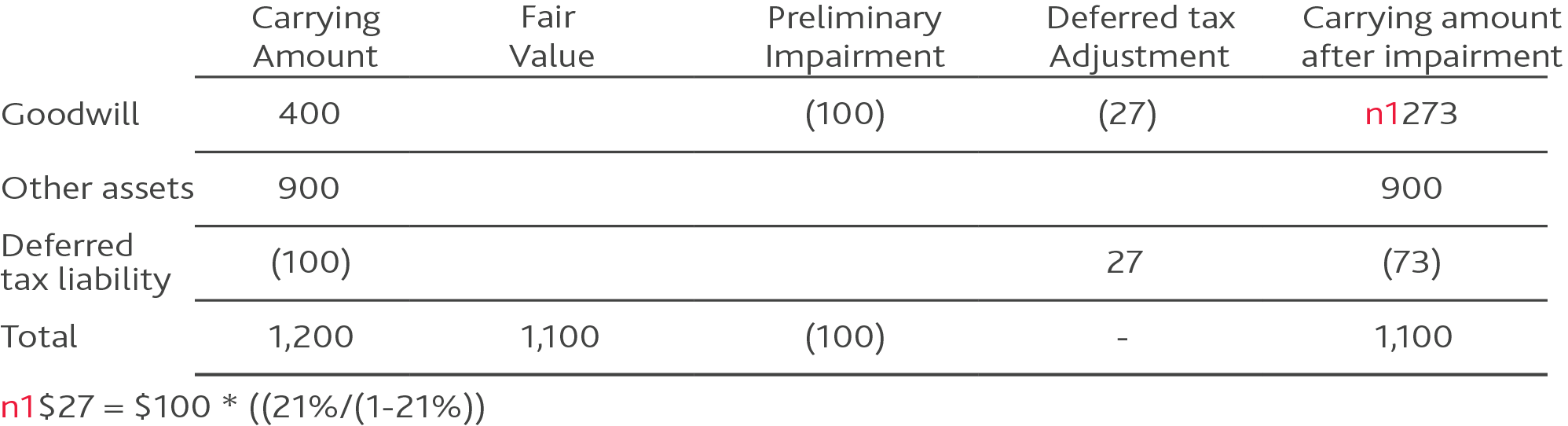

Example – Goodwill Impairment – Tax Deductible Goodwill

In carrying out its annual impairment testing for one of its units, X determined that the fair value of the unit was $1,100 whereas its carrying amount was $1,200. The unit had $400 of goodwill, all of which was tax deductible, a deferred tax liability of $100 related to the Component 1 goodwill and other net assets of $900. X has adopted ASU 2017-04 Intangibles-Goodwill and other (Topic 350) – Simplifying the Test for Goodwill Impairment. The following is the calculation of the impairment based upon the above:

X would report a $127 goodwill impairment charge partially offset by a $27 deferred tax benefit that would be recorded in the income tax line. In cases where tax deductible goodwill exists companies will need to solve the impairment via the use of the simultaneous equation as illustrated above.

Outside basis differences: “Held for Sale” status

COVID-19 has impacted the liquidity of certain enterprises and has necessitated dispositions of assets and businesses to provide needed cash. When the U.S GAAP requirements for “Held for Sale” status have been met, deferred taxes for certain outside basis differences should be considered. In addition, income statement and balance sheet classification of current and deferred taxes will differ depending on the structure of the disposition.

Outside basis differences relate to the difference between the U.S. GAAP and tax basis in the stock of a domestic or foreign subsidiary. Deferred taxes are generally required for such basis differences, although various exceptions apply. For example, deferred taxes are not required for a book-over-tax outside basis difference in a domestic subsidiary if the tax law provides a means of recovering such basis tax-free and the investor intends to utilize that means. In addition, a deferred tax liability is not required for an outside basis difference related to earnings of foreign subsidiaries if such earnings are permanently reinvested.

A deferred tax asset (DTA) for a tax-over-book outside basis in a domestic or foreign subsidiary may be recorded only if it is expected to reverse in the foreseeable future. Foreseeable future is generally viewed a period not to exceed one year.

When an entity is classified as Held for Sale, any unrecorded DTAs or liabilities should be recorded no later than the period in which the Held for Sale criteria is met. It should be noted that Held for Sale status generally meets the foreseeable future standard described above and a DTA should be recorded, subject to realizability. Whether deferred taxes are recorded on outside basis differences will depend on whether the disposition is intended to be a stock sale or an asset sale. In a stock sale, deferred taxes on any outside basis difference should be recorded since the tax gain or loss is computed based on the difference between net proceeds and the tax basis in the stock. In an asset sale, the assets of the subsidiary are being sold and thus the outside book and tax basis amounts are not relevant.

In the period in which the disposition occurs, the balance sheet classification and income statement impacts can differ depending on whether the disposition was a sale of stock or assets. We are aware that there may be diversity of practice in this area.

Finally, where DTAs are recorded for the excess of tax-over-book basis in the stock of a subsidiary, consideration should be given as to whether the stock is a capital asset. Losses on sales of capital assets can only be used against capital gains and can be carried back three years and carried forward five years. Carrybacks are limited where the capital loss creates or increases a net operating loss in the year to which the loss is carried. In cases where capital gains do not exist in carryback years or are not forecasted to be generated within the carryforward period, a valuation allowance should be recorded.

Paycheck Protection Program (PPP) provisions of CARES Act

The PPP provided funds to companies that were significantly impacted by COVID-19 and met specific requirements. Under the PPP, certain loans may be forgiven under specified circumstances in order to promote continued employment and liquidity of the business.

Under Section 1106 of the CARES Act, the loan forgiveness does not give rise to taxable income. However, pursuant to Internal Revenue Service (IRS) Notice 2020-32, expenses that are “allocable” to tax-exempt income are non-deductible. Recently, the IRS addressed in Revenue Ruling 2020-27 the deductibility of expenses funded by PPP loans where the forgiveness has not occurred prior to the end of the tax year in which some or all the expenses funded by the loans were incurred. The IRS concluded that where, as of the end of the year, the taxpayer has not yet obtained forgiveness of the loan but reasonably expects to receive it, the expenses funded by the loans are non-deductible. As of the date of this alert, there have been no enacted law changes that would change the IRS’ position. Congress is currently discussing proposals to allow for the deductibility of expenses funded by PPP loans. Should any of these measures become enacted into law, the impact of the law change would be accounted for periods ended on or after the date of enactment.

The 2020 income tax accounting consequences for PPP funds received in 2020 where forgiveness has not been received by year end (but forgiveness is “reasonably expected” as defined in Revenue Ruling 2020-27) will depend on the pretax accounting model used to account for the loans. The two acceptable models are (a) Debt classification under ASC 470 and (b) Government grant model analogous to IAS 20, Accounting for Government Grants and Disclosure of Government Assistance. The ASC 740 consequences for loans received in 2020 can be summarized as follows:

ASC 470 Debt model

Pursuant to ASC 470, the loan proceeds are classified as debt. The non-deductible expenses funded by the PPP loans and incurred in 2020 are treated as a temporary difference and a DTA is recognized, subject to realizability.

Assuming the loan is forgiven in 2021 and no further non-deductible expenses are incurred in 2021, the 2020 DTA will be written off as deferred tax expense and the loan forgiveness recorded for books in 2021 will be treated as a favorable permanent difference.

Government Grant model

Under this pretax model, a deferred liability account is established when the funds are received, and that amount is released to pretax income as qualified expenses are incurred. For tax accounting purposes, the deferred liability is treated as debt, giving rise to two offsetting temporary differences at the time the funds are received. The income recognized for books in 2020 is not taxable and the expenses funded with the PPP are not deductible.

Assuming the loan is forgiven in 2021 and no further non-deductible expenses are incurred in 2021, the 2020 DTA related to the non-deductible expenses will be written off as deferred tax expense and the deferred tax liability for the tax-over-book basis in the debt will be written off to deferred tax benefit.

It should be noted that the tax accounting consequences outlined above apply only where, as of year-end and under the IRS guidance, it is reasonably expected the PPP loan will be forgiven.

Intra-period tax allocation matters

Taxes are allocated to categories not included in continuing operations (e.g., other comprehensive income (OCI), discontinuing operations, stockholder’s equity) based on a three-step model as follows:

| Step 1: Compute current and deferred taxes on income (loss) in all categories | xxx | |

| Step 2: Compute current and deferred taxes on continuing operations | xxx | |

| Step 3: Subtract step 2 from step 1 -- amount allocated to other category | xxx |

There are numerous exceptions to this three-step model that will result in the tax effects recorded solely to continuing operations. The following are some of these noteworthy exceptions:

Valuation allowances

A change in the valuation allowance for DTAs as of the beginning of the year which results from a change in expectations of income in future years is recorded to continuing operations. Accordingly, even if a DTA was originally recorded to OCI (e.g., related to a change to pension liability) in a prior year, a valuation allowance recorded in 2020 should be recorded to continuing operations.

Changes in tax law and tax rates

The current or deferred impact of changes in tax rates or tax law are recorded directly to continuing operations.

Losses in continuing operations and gains in other categories

Where a company has a loss from continuing operations and gains in other categories (e.g., discontinued operations, OCI) and has a full valuation allowance against its beginning and ending DTAs, a tax benefit will be recorded to continuing operations and tax expense to the other category. This result will provide a different result than the general three-step model outlined above.

ASU 2019-12 removed this exception as part of the FASB’s Simplification Initiative. For a company that early adopted ASU 2019-12, this exception will not apply and the three-step model will be applicable.

Financial statement assertion for outside basis difference

Due to liquidity needs to access foreign cash, some companies may have changed their assertion related to permanently reinvesting earnings of its foreign subsidiaries. Where a company changes its assertion with respect to recording deferred taxes on its outside basis difference in a subsidiary, the tax impact of a change in assertion (relating to the outside basis difference existing at the beginning of the year) is recorded directly to continuing operations.

Valuation allowances

COVID-19 has had a broad and often severe negative impact on the operations of companies worldwide. Companies that are experiencing losses due to the pandemic may need to re-evaluate the realizability of their DTAs. Cumulative losses in recent years, including projected losses in the near term, represent significant negative evidence giving rise to a presumption that a valuation allowance should be recorded. Companies will need to demonstrate that they will generate sufficient taxable income of the appropriate character to utilize their DTAs.

Reductions in the value of investment portfolios may also have occurred due to market volatility. In the case of capital assets where the value of a security is less than its tax basis, a valuation allowance may be needed for DTAs on unrealized capital losses, due to the inability to generate capital gains in current or future periods.

Relief provisions of the CARES ACT may have a positive or detrimental effect on valuation allowance assessments. Specifically, the following provisions should be considered:

- Five-year carryback of tax losses - Losses incurred in 2018, 2019 and 2020 generally may be carried back for five years, which should provide an additional source of income to utilize DTAs.

- Postponement of the 80% taxable limitation on use of loss carryforwards - Losses incurred through 2020 and that are utilized before 2021 generally are not subject to the 80% taxable income limitation.

- Interest deduction limitations - For tax years 2019 and 2020, the Internal Revenue Code Section 163(j) limit of 30% of adjusted taxable income (ATI) generally is increased to 50% of ATI, at the taxpayer’s election. This may allow more interest to be deductible, thereby reducing interest carryforwards subject to a valuation allowance. Further, a company’s 2019 ATI limitation may be substituted for the 2020 ATI limitation, and special rules were enacted for interest expense of partnerships, also resulting in higher interest deductions.

Final Treasury regulations were issued in 2020 under Section 163(j) and the GILTI provisions of Section 951A that could impact valuation allowance assessments. For example, the Section 163(j) regulations do not treat certain financing-related costs, such as loan commitment fees, as interest expense for section 163(j) purposes. This favorable change can be, at the taxpayer’s election, applied retroactively to 2018. This may result in increased interest deductions, thereby reducing interest carryforwards otherwise requiring a valuation allowance.

Final GILTI regulations issued in 2020 contain a “high tax exclusion” whereby foreign earnings subject to a foreign tax rate of at least 90% of the U.S. tax rate can be excluded from U.S taxable income. Like the Section 163(j) regulations, this provision can be elected retroactively to 2018. Election of the high tax exclusion will eliminate a source of income for utilizing DTAs and could negatively impact a valuation allowance assessment.

As a result of the 2017 U.S. tax legislation and the significant tax developments in 2020, scheduling of existing taxable and deductible temporary differences is as important as ever. Certain companies that have persuasive negative evidence such as cumulative losses in recent years and must rely solely on scheduling of existing temporary differences, may need to modify such analysis to consider the 2020 tax developments, including items discussed herein. There have been questions concerning what sources of income should be considered when determining whether interest carryforwards are realizable. There are four sources of income that are considered in evaluating the realizability of DTAs:

- Taxable income in prior carryback year(s) if carryback is permitted under the tax law

- Future reversals of existing taxable temporary differences

- Tax-planning strategies

- Future taxable income exclusive of reversing temporary differences and carryforwards

Each source of income should be considered incrementally to determine whether a valuation allowance is needed for interest carryforwards. If one source of income is sufficient to utilize such carryforwards, no other source of income should be considered.

For example, when scheduling the future reversals of existing temporary differences (source 2 above), if the interest carryforwards are utilized, subject to the 30% or 50% ATI limitations, a valuation allowance should not be recorded. The fact that the company expects its future interest deductions to be limited by IRC Section 163(j) is not relevant, since its existing carryforwards can be realized by future reversals of existing temporary differences. This fact pattern was addressed by the AICPA in its Technical Questions and Answers (TQA) – Section 3300 Deferred Taxes.

Global COVID-19 tax relief measures

To help companies deal with the economic fall-out of COVID-19, governments around the world have enacted both tax and non-tax relief measures. Companies should analyze these measures to determine if the tax impacts should be accounted for as income taxes under ASC 740, government grants, loans or contributions. Some of the relief measures, such as enhanced tax depreciation, additional loss carryback and carryforward periods, and tax deductions for COVID-19-related investments, are clearly accounted for as income taxes under ASC 740. Other changes such as income tax credits will ordinarily be accounted for under ASC 740, but credits allowable against non-income taxes (e.g. payroll tax credits) would generally not be accounted for as income taxes. It should be noted that if a tax credit can be used to offset tax on taxable income, then it would generally be accounted for under ASC 740. Alternatively, refundable credits that cannot offset a company’s income tax liability are generally not accounted for under ASC 740.

Many incentives enacted as a result of the pandemic are unique, so careful analysis should be taken to properly determine the accounting model to apply.

SHARE