Employee stock ownership plans (ESOPs) have become an increasingly compelling exit strategy for business owners, offering unique flexibility, potential tax advantages, and long-term benefits. While ESOP sales might provide less cash upfront compared to private equity or strategic mergers and acquisitions (M&A) deals, recent trends show the liquidity gap is narrowing, and legislative support continues to grow. A well-structured ESOP, especially in a 100% S corporation ESOP transaction, can provide structural flexibility to achieve the goals of the company and selling shareholders. Business owners selling stock to an ESOP have options in how to finance the ownership transition.

This article outlines borrower consideration, ESOP financing capital sources and structures, and how to pursue favorable financing terms through a competitive capital raise process.

Assessing Liquidity Goals and Determining Suitability

The first decision is whether to borrow funds from an independent capital provider or seller-finance the deal. Banks and financial institutions have increasingly recognized ESOPs as viable borrowers, largely because of the low default rates observed and potential tax advantages afforded to ESOP-owned companies. According to the National Center for Employee Ownership (“NCEO”) a study tracking the entire population of ESOP companies over 10 years found that privately held ESOP companies were half as likely as non-ESOP firms to go bankrupt or close and three-fifths as likely to disappear for any reason.

A company’s ability to borrow outside capital starts with the five “Cs” of credit.

- Character – borrower’s credit history and reputation. Offering materials should clearly present the company’s credit profile, transaction rationale, and overall ESOP investment thesis to a targeted group of prospective lenders.

- Capacity – borrower’s ability to repay the loan based on earnings and capital obligations. Financial modeling can help evaluate the preferred credit structure (e.g., term loan versus asset-based lending) and assess the company’s debt capacity under both base case and downside scenarios while also considering the company’s appetite for debt.

- Capital – borrower’s own financial investment in the deal. At some level, part of the equity value sold to an ESOP will be seller-financed, tying a portion of the seller’s proceeds to the company’s future performance. Finding the right balance between valuation and financing is crucial to any successful leveraged buyout. Seller notes may be structured to accommodate senior bank subordination requirements while achieving returns that align with subordination risks.

- Collateral – borrower’s security to the loan. The amount and type of collateral available affects the total credit commitment and terms. Setting realistic expectations up front can help companies and selling shareholders evaluate available financing alternatives.

- Conditions – borrower’s risk and economic environment; loan terms. Senior financing availability will vary by lender; industry; market conditions; and company-specific factors, including industries that might be viewed as more challenging from a credit perspective, such as general contractors.

The company’s business model affects how the credit will be structured. For example, a manufacturer with significant inventory and equipment might borrow against its collateral base on a line of credit to partially finance the ESOP transaction. Typically, asset-based lines of credit have more flexible subordination requirements against the ESOP seller note compared to a cash flow loan. A service-based company with minimal assets will typically require a cash flow lending structure collateralized by its earnings before interest, taxes, depreciation, and amortization (EBITDA). Banks consider cash- flow loans as riskier, given the collateral shortfall. As such, cash flow loans typically have stricter subordination requirements for the seller note.

Businesses that want to transition ownership to an ESOP and not borrow outside debt can finance the sale through seller notes. And whether the company sells 100%, a minority position, or somewhere in between, the prudent lending structure will balance liquidity, risk, returns, and flexibility. The following section outlines the types of credit providers.

Senior Tranche

ESOP financing demands a deep understanding of long-term cash flows, repurchase obligations, the seller note component, and how the senior bank might provide support above and beyond the loan to finance the ESOP sale. Many large banks and even regional banks have dedicated ESOP teams consulting with local bankers and credit committees on ESOP transactions. Those dedicated resources can help streamline responses and can improve the efficiency of the approval process.

Typical Senior Bank Terms:

- Term or maturity period is typically five to seven years. The company may have the ability to refinance the debt during the life of the loan or at maturity.

- Amortization periods range from five to ten years. Longer amortization periods favor the borrower.

- Variable interest rates tied to the secured overnight financing rate (SOFR) plus a margin. The margin can range from 1% to 2.5% depending on risk and repayment source (e.g., future EBITDA or assets). Companies might want to hedge interest rate risk through an interest rate swap, and a senior lender might require a company to hedge some portion of the loan.

- Excess cash flow recapture is a common feature for cash flow loans. The excess cashflow provision is not meant to be punitive or preclude strategic investments or capital expenditures. That structure gives the senior lender confidence that any residual cash flow, after all debt service and capital investments, is used to prepay the senior debt within the stated maturity period. Often, companies in the early years will use any excess cash flow to prepay the debt anyway.

- Senior lenders will take priority and first lien positions on the company’s assets as security. Senior banks typically require the company to maintain deposits and treasury management to offset costs of capital.

- Negative covenants are promises by the borrower not to do specific things without approval or to maintain financial covenants, such as a fixed-charge coverage ratio (FCCR) and senior leverage ratios. The FCCR monitors how much cash is available to service debt and the senior leverage ratio monitors how much senior debt is outstanding relative to EBITDA. Each provides a direct metric for banks and borrowers to assess financial health.

In a 100% sale to an ESOP, it is typically not practical for a senior bank to fund the entire purchase price, given credit policy and amortization requirements. If the sellers do not want to take back a large seller note as a form of consideration, other forms of alternative capital can bridge the liquidity gap.

The type and source of alternative capital depend on several items, such as company size and earnings capacity, amount of capital needed, cash flow and collateral coverages, ownership objectives, and equity allocation among the parties.

Types of Alternative Capital Providers

- Mezzanine Lenders: Includes banks, private equity, specialty firms, or hedge funds that typically seek higher returns and might require synthetic equity or board seats.

- Private Credit: Might support initiatives such as expansion, buyouts, or corporate restructuring. These capital providers may offer flexible financing structures tailored to the specific needs of the business and can often contribute operational expertise. ESOP transaction example: BDO USA’s ESOP transaction was partially financed through private credit.

- Non-Bank Financial Institutions: Insurance companies, pension funds, etc., that offer loans and credit but are not regulated like banks. ESOP transaction example: A global manufacturer of premium consumer goods completed a 100% ESOP conversion that was financed in part by institutional investors, including a pension plan and an impact investor, demonstrating how alternative capital can support employee ownership transactions.

Before delving into the types of alternative capital structures, it is important to understand the components of how returns are structured:

- Cash pay interest – paid at least quarterly; variable rate tied to SOFR or prime plus a spread

- Payment-in-Kind (PIK) Interest – accrues and compounds rather than being paid in cash; less common in unitranche structure

- Fees – origination, commitment, and exit fees enhance returns

- Equity Return – preferred stock, warrants, or other equity participation

Types of Alternative Capital Structures

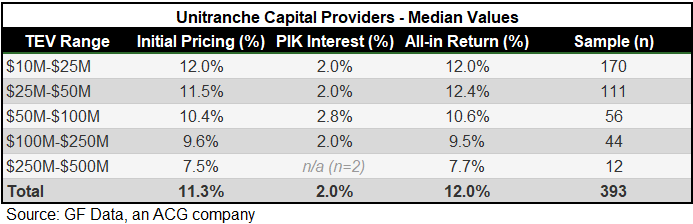

Unitranche Debt – A single-layer financing structure that combines senior and subordinated debt into one instrument, simplifying the borrower’s capital structure. It is commonly used in middle-market leveraged buyouts and recapitalizations because it reduces complexity and might accelerate closing compared to having separate senior and mezzanine tranches.

Key Characteristics of Unitranche Financing:

- Single Loan Agreement: Simplifies negotiations and legal documentation for the borrower.

- Blended Interest Rate: The rate is higher than traditional senior debt but lower than mezzanine debt because it combines both risk profiles.

- Behind the Scenes: Lenders often enter into an agreement among lenders to split economics and priority internally (first-out versus last-out tranches).

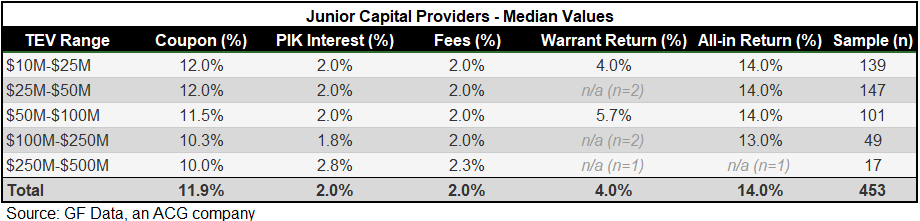

Junior Capital – financing that sits below senior debt in the capital structure but above common equity. Junior capital can take the form of mezzanine debt, preferred equity, or a hybrid structure.

Key Characteristics of Junior Capital:

- Subordination Position: Junior capital ranks behind senior secured debt in repayment priority.

- Higher Risk, Higher Return: Because it is junior to senior debt, junior capital commands a higher yield and often includes equity participation.

- Flexible Structure: Can be structured as debt with equity kickers or as preferred equity with fixed dividends.

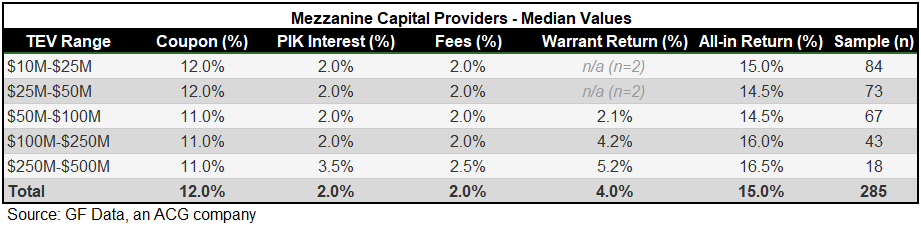

Mezzanine Capital – A hybrid form of capital that sits between senior debt and equity in the capital stack. It is commonly used in leveraged buyouts, recapitalizations, and growth financing when a company needs additional capital beyond what senior lenders will provide but wants to avoid diluting ownership too much with pure equity.

Key Characteristics of Mezzanine Financing:

- Subordinated Debt: Mezzanine debt ranks below senior secured debt but above equity in priority of repayment.

- Unsecured or Lightly Secured: Typically not backed by significant collateral.

- Higher Risk, Higher Return: Because mezzanine financing is junior to senior debt, it carries more risk and therefore commands a higher return.

Even with a growing set of non-bank lenders and structures, alternative capital is still used less frequently in ESOP transactions than in the broader M&A market. Third-party junior capital typically comes into play when sellers want to increase cash at closing and reduce the amount of proceeds deferred into a seller note. Common reasons owners might choose not to pursue alternative capital include:

- Outside capital can be more expensive than seller financing.

- Reservations about adding new financial partners, sharing confidential information, or providing board seats.

- Sellers in an ESOP might prefer to receive that attractive return themselves while continuing to operate the company.

Seller Note in an ESOP Transaction

A seller note (akin to junior capital) is a form of financing commonly used in ESOP transactions to bridge the gap between the total purchase price and the amount funded by senior lenders or other capital sources. In that structure, selling shareholders agree to receive a portion of the sale proceeds over time rather than all cash at closing. The seller note is typically subordinated to senior debt, meaning it is in second position and repaid after the senior lender is paid in full.

Key features of seller notes in ESOP deals:

- Flexible Terms: Seller notes can be structured with flexible repayment schedules and interest rates and might include features like warrants to yield a market rate of return that reflects the inherent risk of junior capital.

- Lower Cost: Compared to junior or mezzanine capital, seller notes can be less expensive when considering time-value-of-money factors and have more favorable terms for the company.

- Alignment of Interests: Because repayment depends on future company performance, seller notes often include incentives for the seller to support the ongoing success of the business. The warrants also align the seller with the ESOP participants.

- Subordination: Seller notes are subordinate to senior bank debt, meaning they are repaid only after the senior lender’s obligations are satisfied or as the senior lender allows.

- Liquidity Bridge: They provide a way for sellers to realize additional liquidity when senior lenders cannot finance the entire transaction, especially in 100% ESOP sales.

Sellers are often more flexible than third-party lenders, and the terms can be negotiated to suit both the company’s and the seller’s needs.

Evolving Trends in ESOP Financing

The Small Business Administration (SBA) lending program has played an increasingly important role in financing ESOP transactions, especially for small and mid-sized businesses seeking upfront cash proceeds to partially finance the ownership transition. Recent regulatory changes have made SBA-backed loans more accessible and attractive for ESOPs in some circumstances.

The American Ownership and Resilience Act, proposed in both chambers of Congress in May 2025, would create a zero-subsidy investment facility administered by the Department of Commerce. The facility would provide loan guarantees for private investment funds focused on expanding employee ownership among small and mid-size businesses. The act is intended to make ESOP financing more accessible by reducing barriers and streamlining the process.

Capital Raise Process Considerations in an ESOP Transaction

A debt capital raise process often runs in parallel with the broader transaction timeline. In many ESOP transactions, the financing workstream includes preparing the confidential information memorandum, identifying prospective lenders, coordinating diligence, comparing indicative terms, and advancing documentation through closing. A structured process can help companies evaluate financing alternatives considering structuring, pricing, covenants, flexibility, execution requirements, and timing.

How BDO Capital Advisors Can Help

Navigating ESOP financing requires careful consideration of transaction structure, capital sources, lender requirements, and long-term business objectives. For companies evaluating an ESOP as an ownership transition strategy, it is important to work with advisors who understand the complexities of ESOP transactions and the financing options available.

BDO Capital Advisors’ ESOP Advisory team can help companies assess financing alternatives, evaluate transaction structures, and navigate the capital raise process in support of a successful ownership transition. If you are considering an ESOP, contact BDO Capital Advisors to discuss how financing strategies can align with your business goals.

GF Data Footnotes:

- Data source: provided by GF Data, an ACG company.

- Dataset: January 1, 2020, through December 31, 2025.

- Data filter: Total Enterprise Value >$20 million, EBITDA >$5 million.

- Junior Debt: Transactions submitted by non-mezzanine contributors (PE groups, family offices, independent sponsors) with leverage type "Senior and Subordinated Debt." The subcomponent represents junior capital arranged as part of the sponsor's capital structure.

- Initial Pricing (%): Reflects the all-in pricing (SOFR + spread) at transaction close.

- Coupon (%): Reflects all-in coupon (base rate + spread) at transaction close.

- Warrant Return (%): Warrant-based return represents the expected annualized gain, expressed as a percentage, so it can be added to the other cost-of-capital components. Per GF Data methodology, submitters calculate this using the junior capital provider's expected holding period.

- All-in Return (%): The All-in Return average is drawn from deals that reported a complete all-in figure, while the individual components each have different sample sizes.

- Items Not Tracked: Preferred dividends and equity participation. Warrant-based return is the closest proxy for equity participation.

Investment banking products and services within the United States are offered exclusively through BDO Capital Advisors, LLC, a separate legal entity and affiliated company of BDO USA, P.C., a Virginia professional corporation. For more information, visit www.bdocap.com. Certain services may not be available to attest clients under the rules and regulations of public accounting. BDO Capital Advisors, LLC Member FINRA/SIPC.