BDO Technology Outlook Survey

About the Survey

The 2019 BDO Technology Outlook Survey is a national telephone survey conducted by Market Measurement, Inc., an independent market research consulting firm, whose executive interviewers spoke directly to chief financial officers (CFOs). Market Measurement used a telephone survey performed within a scientifically developed, pure, random sample of U.S. technology companies in the software, hardware, telecommunications, internet, and information technology services subsectors.

Introduction

Can the U.S. technology industry maintain its momentum through 2019?

U.S. tech companies dominated the spotlight last year, drawing attention from governing bodies, organizations, and consumers around the world.

To many, the sector has never soared so high. New products, services, and business models championed by tech companies are disrupting entire industries. Rapid advancements in artificial intelligence, cloud computing, data analytics, and other emerging technologies are revealing additional glimpses of the future. Meanwhile, technology’s prolific adoption around the world shows no signs of ceasing.

Tech is, more or less, touching everything.

But there is a flip side. While some have eagerly watched tech’s rise, others have started to wonder whether the industry is flying too close to the sun. The idea that unregulated ambition has led certain tech companies to become too influential is not uncommon, nor the concern that their products and services may have unintended consequences.

So, what will 2019 bring?

Will the U.S. tech sector—one of the S&P 500’s leading performers in 2017 and last year—continue to ride the wave of enthusiasm to generate exponential growth? Or will it face an economic slowdown?

The answers are mixed, according to the 100 U.S. tech CFOs surveyed in BDO’s 2019 Technology Outlook Survey. While the U.S. economy remains strong, trade wars, tax reform, data privacy concerns, and other geopolitical tensions and policy changes threaten to shake up the sector. Meanwhile, increasing competition at home and abroad, along with evolving customer expectations, make innovating and scaling up quickly and sustainably an absolute imperative.

“Tech companies must prepare for continued regulatory and international trade uncertainty in 2019 by re-evaluating and fortifying their operational and financial management. By establishing a strong foundation, organizations will be better positioned for growth amid any potential headwinds.”

.jpg "2018-Technology-Outlook-Survey1_Jamil-(1).jpg")

Aftab Jamil

Assurance Partner and Global Technology Practice Leader

![]() Scale Up

Scale Up

Spearheading & Funding Innovation

Technological innovation—the phrase of the decade.

To find a company today that doesn’t have innovation on its radar would be nearly impossible; the process has become so synonymous to growth in the 21st century that any organization ignoring it doesn’t stand a chance.

As a result, product or service innovation is the second- most highly cited business priority among tech CFOs.

Scaling the business is #1.

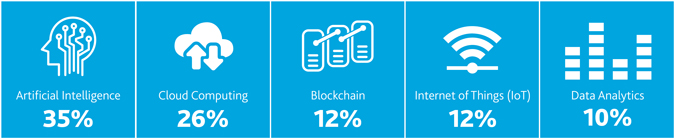

Technologies Anticipated to Cause the Greatest Industry Disruption in 2019

.jpg "TECH_Outlook-Survey_2019_technologies_graphic-x675-(1).jpg")

To achieve their growth objectives, many tech companies are looking to recruit and retain critical talent (34 percent)—a top challenge in today’s tight labor market. Other strategies include adding new products or services, pursuing mergers and acquisitions (M&A), expanding in emerging markets, and seeking additional capital.

Among those planning to seek additional capital this year, fundraising through private debt remains the most popular choice.

Tech companies are optimistic their efforts will pay off: 84 percent expect an increase in total revenue this year, with an average net change of 12.7 percent—slightly higher than the estimated 12.2 percent change in 2018 and the highest recorded in the study’s history.

Bridging the Tech-Talent Gap

An organization is only as strong as its people.

As such, more than a third (34 percent) of tech CFOs cite recruiting and retaining talent as the most important strategy in achieving their growth objectives over the next two years.

However, a huge technology talent gap remains despite companies’ best efforts to close the divide via training programs, tech apprenticeships, and more. The challenge to recruit workers with relevant technical skills, while addressing diversity, is a significant one.

While a lack of high-tech skills is a key contributor to the talent shortage, another factor is shifting immigration policy. While most executives (59 percent) harbor low or no concerns about immigration, international talent remains a key part of the U.S. tech industry. Any policy changes—including changes to the H-1B visa program—can have significant repercussions on talent management.

62% of tech companies expect an increase in their number of employees this year.

31% expect their workforce size to stay the same.

From 2016-2026: Employment of computer and IT occupations is projected to grow 13%—faster than the average for all occupations.

Demand for these workers will stem from greater emphasis on:

-

Cloud Computing

-

Collection & Storage of Big Data

-

Information Security

► The economy will need as many as 100,000 new IT workers per year over the next decade.

► Right now, only about 60,000 enter the workforce each year.

*Source: U.S. Bureau of Labor Statistics

Scaling Through Collaboration: M&A Outlook

Another core strategy to scaling is through mergers and acquisitions (M&A).

Riding on last year’s robust M&A activity, tech CFOs continue to have hopeful expectations for 2019: 55 percent expect M&A activity to increase—out of which, 16 percent expect it to increase significantly. The same goes for valuations, with 43 percent expecting an increase, despite the fact that many have already reached sky-high amounts.

Because of these ripe market conditions, 60 percent of companies expect to pursue M&A in 2019.

What’s Driving U.S. Tech M&A?

The Formidable State of the Capital Markets

U.S. tech is enjoying—and will likely continue to enjoy—a coalescence of high corporate profitability, record-high equity valuations, and positive business sentiment. Expansionary fiscal policy has stoked the balance sheets of tech companies, as large global players are repatriating cash at lower rates. Massive stores of cash and high public valuations are creating fuel for dealmaking. This capital, if left on tech companies’ balance sheets, will erode shareholder value. Repurchasing stock is a simple solution to cash windfalls, but capital deployment into M&A offers a high-yielding investment alternative.

Digital and Technology Disruption

No industry is immune to the competitive pressures emanating from digital and technological disruption. Industries are converging globally, and companies need to constantly re-assess whether they can sustain their competitiveness. Cloud storage, cloud security, business intelligence, data analytics, and other technologies are imperative capabilities for any business; companies are pursuing business in these sectors to address digital transformation, accelerate innovation, and develop products that confront disruption within their industries. As a result, valuations of these companies continue to rise.

A Year of Unicorns? IPO Outlook

Can 2019 match 2018’s strong year for IPOs?

The answer seems to be leaning favorably toward “yes”—but tech CFOs are balancing optimism with caution.

First, the optimists: 37 percent of tech CFOs believe U.S. tech IPO activity in 2019 will increase this year, and 46 percent expect it will stay the same—in other words, quite high. Despite the turbulent market that shook up investors and businesses at the end of 2018, a robust pipeline of mega-unicorns holds ample promise for the year ahead.

Nevertheless, a slew of unknowns still exists. The 35-day-long federal government shutdown—and temporary ceasing of the U.S. Securities and Exchange Commission—at the beginning of 2019 has forced many unicorns to stall their IPO plans. Meanwhile, a volatile stock market and fears of a possible recession have fostered growing skepticism and unease among investors and companies, leading some executives to harbor second thoughts.

In addition, going public may no longer be the most attractive option for high growth companies looking to take the next step. As opposed to doing an IPO in the U.S. or a foreign market, most tech CFOs expect that pursuing M&A instead will be the most popular “exit strategy” among private U.S. tech companies in 2019, followed by staying independent.

Build Up

Tax Reform Top of Mind

Sixty-eight percent of tech CFOs harbor high or moderate concerns about tax changes in 2019.

Domestic tax issues naturally reign, followed by those abroad.

U.S. Tax Reform Looking Favorable

While the new U.S. tax reform law has been in place for over a year now, 2019 will be when tech companies truly feel its impact.

What will its effect be? Three-fourths of tech CFOs expect it to have a favorable impact on the industry this year—with nine percent expecting a “very favorable” impact. This may be attributable to provisions like the lowering of the corporate tax rate and the ability to repatriate overseas cash at a lower tax rate, among others.

Nevertheless, not all are convinced of tax reform’s benignity. One-fifth expect it to have a “somewhat unfavorable” effect on tech companies this year, which could be due to unforeseen consequences that may not emerge until years later. For the time being, most survey participants don’t expect to significantly change their current business practices to accommodate.

In response to tax reform, tech companies in 2019 will or will not take the following actions:

The EU’s Digital Tax On The Horizon

Tax compliance in multiple jurisdictions is a key worry for 22 percent of tech CFOs. Among these is a proposed tax from the European Commission that could cost U.S. tech companies billions of dollars. Championed by French President Emmanuel Macron, this plan proposes a 3 percent digital tax on companies with annual global revenues of at least €750 million ($851 million) and online sales of €50 million ($56.8 million) in the European Union.

Unlike the current tax system, the digital tax would focus on taxing revenue generated in the region versus profits. If enacted, it could go into effect as early as 2020.

Meanwhile, the United Kingdom has already announced its own version: a 2 percent levy on sales of digital services in the U.K., to take effect April 2020. Even more countries are following the EU’s lead, including South Korea, India, and several Asian-Pacific countries, along with Mexico, Chile, and other Latin American nations.

Navigating South Dakota v. Wayfair’s Tax Code Changes

In June 2018, the U.S. Supreme Court issued its widely anticipated decision in South Dakota v. Wayfair. In what is likely the most significant state tax decision in more than 50 years, the Court held that the physical presence rule for state tax jurisdiction is incorrect and not a requirement under the Commerce Clause of the U.S. Constitution.

While the South Dakota v. Wayfair decision may not rank as high a priority for CFOs as tax reform (10 percent), it nevertheless has significant implications for technology product companies, including those offering software, online services, software-as-a-service (SaaS), gaming, digital media and content, streaming, information, and data processing, among others. Overnight, it changed a remote seller’s considerations from, “Do I have a physical presence?” to “How do I comply with all of the state and local jurisdictions where I deliver my products or services?”

As a next step, tech companies should determine the specific rules they are subject to under each taxing jurisdiction. Next, they should assess if their current sales and use tax systems and controls are robust enough to comply with these requirements. Now may be a good time to consider tax automation solutions to ensure compliance with state and local laws, and to more efficiently report and remit taxes.

“U.S. tax reform, along with significant tax code changes at the global and state and local levels, will continue to have ripple effects on tech companies for years to come. As a result, tech companies will have to ensure that they’re not only up-to-speed with the latest tax policy updates, but that they are constantly redefining their tax strategy to manage future risks and opportunities that come with the tech industry’s continued impressive growth.”

.jpg "2018-Technology-Outlook-Survey_headshots3_Yasukochi-(1).jpg")

David Yasukochi

Tax Office Managing Partner and Technology Practice Co-Leader

Accounting Deadlines Loom

Revenue Recognition

In May 2014, the Financial Accounting Standards Board (FASB) issued ASU 2014-09, Revenue from Contracts with Customers (Topic 606), otherwise referred to as the new revenue recognition standard. ASU 2014-09 establishes comprehensive accounting guidance for revenue recognition and replaces substantially all existing U.S. GAAP on this topic.

Revealing a somewhat troublesome trend, only 65 percent of survey participants have taken actions to implement the new standard, leaving 35 percent to do so. Given that the deadlines for public and private companies have already passed, those that fall into the latter category risk significant repercussions for a lack of compliance with the U.S. GAAP requirements for financial reporting.

Deadlines:

► Public Entities: Jan. 1, 2018

► Private Entities: Annual reporting periods after Dec. 15, 2018

Lease Accounting

In February 2016, the FASB issued its leasing standard in ASU 2016-02, Leases (Topic 842), otherwise referred to as the new lease accounting standard. The new standard establishes accounting guidance for both lessees and lessors and will affect every entity that leases property, plant, or equipment.

Companies with large operating lease obligations—such as facility leases—will likely feel the most impact, as well as startups and mid-sized businesses that rely on leasing instead of purchasing equipment due to tight budgets. How heavy a compliance burden an entity faces will depend significantly on how well it has tracked its lease transactions and assets to date.

Only 39 percent of survey participants have taken actions to implement the new lease accounting standard, leaving 61 percent to do so. Out of this 39 percent, 47 percent are public companies, and 33 percent are private. Private companies have less than a year to comply.

Deadlines:

► Public Entities: Jan. 1, 2019

► Private Entities: Fiscal years after Dec. 15, 2019 and interim periods within fiscal years after Dec. 15, 2020

Armor Up

Data Privacy & Cybersecurity

Cybersecurity concerns, along with U.S. economic growth, will be the top drivers of U.S. tech industry growth in 2019, according to survey participants.

Chief among those concerns is data privacy, with 87 percent expressing a high or moderate concern about the issue. Last year’s Facebook-Cambridge Analytica data scandal, among others, was a sobering reminder of the stark reputational, financial, and legal consequences that can follow the negligence of personal data.

As a result, policymakers around the globe are quickly modernizing data protection laws for today’s fast-paced, digital environment—starting with the EU’s General Data Protection Regulation (GDPR), which came into effect May 2018. Privacy concerns are much farther reaching than in the past, ranging from bad actors to authorized users. Even the latter may be in violation when the original intent of collecting, processing, transferring, or storing personal data changes.

Despite the dangers, more than half of tech CFOs (53 percent) are very confident about their organization’s ability to detect a data breach. Could they be overconfident? Protecting personal data extends far beyond setting up basic internal security controls today; companies would do well to follow seven foundational principles.

The 7 Foundational Principles of Privacy by Design

|

1. Proactive, Not Reactive; Preventative, Not Remedial |

|

|

|

2. Privacy as the Default |

|

|

|

3. Privacy Embedded into Design |

|

|

|

4. Full Functionality |

|

|

|

5. End-to-End Security |

|

|

|

6. Visibility and Transparency |

|

|

|

7. Respect for User Privacy |

Overseas Competition & China Concerns

Of the five countries listed, China is expected to pose the greatest competitive threat to U.S. tech in 2019 (73 percent), followed by India (17 percent).

The U.S.-China trade war, which has resulted in tariffs on approximately $250 billion dollars’ worth of Chinese goods as of December 2018—and Chinese tariffs on an estimated $110 billion worth of U.S. goods—has led 65 percent of CFOs to harbor high or moderate concerns about trade policy changes. With much uncertainty ahead, U.S. tech companies, with their extensive supply chains and operations in China, have ample cause for concern.

The technology race between the U.S. and China also shows no signs of slowing down. Boasting some of the world’s biggest tech companies, including Alibaba, Tencent, and Baidu, China’s tech landscape has seen exponential growth over the past decade. Whether its tech industry will eventually supersede the U.S.’ in economic prowess and influence is yet to be seen—but such a future is no longer impossible.

“The year ahead will be a challenging time for the relationship between the U.S. and China tech industries. Tariffs from both countries have contributed significantly to pricing pressures and supply chain disruptions. Meanwhile, tighter U.S. export controls on sensitive emerging technologies and increased delays of various approvals in China for U.S. businesses, among other issues, are real causes for concern for many U.S. tech executives.

However, American companies should not be too keen to exit operations from the country. China still commands enormous opportunities for U.S. companies and will likely continue to do so for some time to come. The relationship’s current uncertainty mandates companies’ patience—this is a long game, not to be played with haste.”

Johny Chalklader

Johny Chalklader

Export Controls and International Trade and Regulatory Affairs Practice Lead, BDO’s Industry Specialty Services—Government Contracts Group

Antitrust Regulation

Most tech CFOs (71 percent) express low or no concerns about antitrust regulation, but that doesn’t mean it’s not significant.

Big tech, especially, has reasons to be cautious. Besides already experiencing a slew of antitrust proceedings last year, U.S. tech companies are having to answer to authorities in international jurisdictions that are growing increasingly wary of the consumer data they have access to. Public concerns about whether certain tech giants have grown too big and influential across all aspects of society—from driving consumer behavior to influencing politics—also continue to resound.

Conclusion

2019 will be a pivotal year for U.S. tech.

While a strong U.S. economy, cybersecurity concerns, consumer demand, and digital transformation promise to drive industry growth, significant changes to trade, tax, antitrust, immigration, and other regulations threaten to shake up any notions of smooth sailing. Tech companies have a lot on their plate, but with enough foresight and preparation, their goal to Scale Up, Build Up, and Armor Up sustainably and successfully this year and beyond can still be within reach.

SHARE