Acting on Our Audit Quality Intent

Any structure is only as strong as its foundation. The initiatives discussed in this report are supported by the many investments in time, energy, and resources we have made over many years to create and sustain a best-in-class organization at BDO.

Our work in building an auditing practice that continually stays at the leading edge of our clients’ needs and the industry’s demands will never be finished. In 2017 and into 2018, we continue to sharpen our focus on performance management and accountability, with an emphasis on further enhancements to our audit approach and the development of our professional skepticism framework. In addition to these and other initiatives, we continually improve in other areas of our operations. In particular, we are committed to expanding our skillsets and adding the leadership necessary to bring a fresh perspective to the challenges facing the audit industry and our clients.

Expanding the Reach of our National Assurance Office

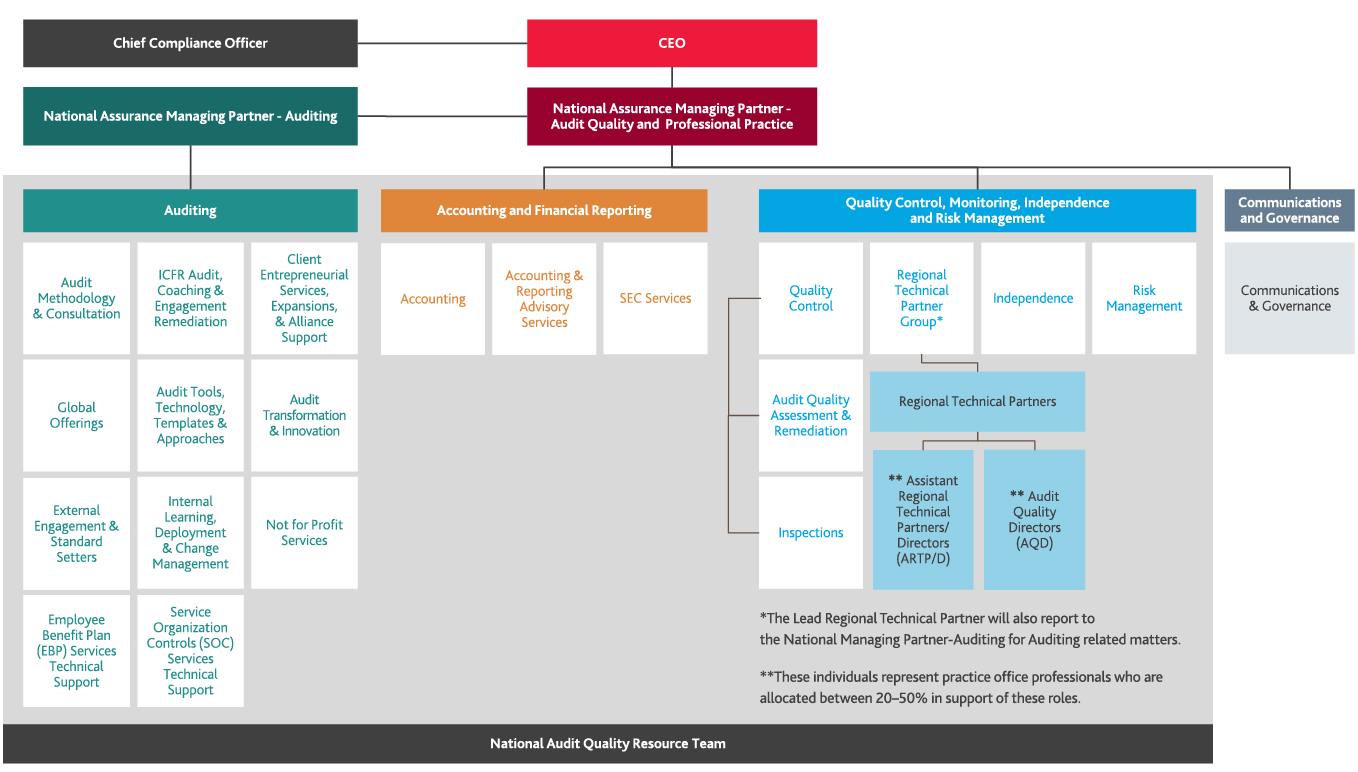

BDO’s National Assurance Office is the centerpiece of ensuring our continued excellence in audit. The resources we have invested in National Assurance have led to an increase in staff of 74% since 2014, which has helped to transform the office into a hub for all of our audit quality efforts to benefit both our clients and our entire Assurance practice. National Assurance further serves as a clearinghouse of consultative and technical knowledge, professional coaching and development support, and education. This group also plays a major role in innovation, monitoring, and accountability.

National Assurance Organization

BDO’s National Assurance has been defined along operational areas overseen by our National Assurance Managing Partner of Audit Quality and Professional Practice, who directly reports to BDO’s Chief Executive Officer. This reporting structure helps to ensure that our CEO is directly dialed into audit quality processes and is better able to operationally support and convey important messaging about audit quality expectations to all of our BDO professionals.

.jpg "BDOorg-2x-(2).jpg")

Click the image to view larger version.

We have also made important changes to the operational audit areas overseen by National Assurance. This demonstrates how seriously we take our commitment to our clients and our client-serving professionals.

Click on a tab below to learn more.

.png "Actingontabs_4.png")

Promoting Audit Quality at the Engagement and Firm Levels

At BDO, we measure audit quality at both the client engagement level as well as the firm level.

Audit Milestones

Recognizing the impact on audit quality of an orderly, timely, and sequenced audit process that occurs over a predictable time period, we follow a series of audit milestones when executing our audits. The use of audit milestones forces discipline into and throughout the audit process by fostering earlier risk identification and assessment. This, in turn, enables appropriate planning, design, and performance of audit work in a sequence to allow more structured time for areas requiring significant judgment.

Engagement Support

Issuing an audit opinion is an enormous responsibility. To support audit teams in performing a high quality audit that provides confidence to those who rely on our report, we require all audit teams to engage in activities which continually reassess and reaffirm the design of the audit and its effective execution. For example, engagement teams reconsider their risk assessments and audit response designs prior to concluding the audit to confirm that decisions made earlier in the audit cycle remain relevant. Our coaching programs, which leverage professionals from the National Assurance Audit Quality Team, provide audit teams with real-time feedback on risk assessment and audit execution.

In providing support to non-issuer audits, we intentionally align and distinguish resources—professionals, policies, tools and templates, education and methodology—to be distinctive in the work we do on private company audits. For example, our Private Company Audit Innovations (PCAI) team continually surveys our auditors to identify opportunities to increase efficiencies without sacrificing quality through streamlining, standardizing, and focusing audit procedures, while simultaneously ensuring adherence to relevant AICPA auditing standards. Efforts by the PCAI team emphasize differentiation and modification from public company engagements, with a focus on audit tools, guidance, and education for private company audit engagement teams. This will continue to be a key priority as our PCAI team accelerates its work this year.

Quality Control System

Turning our own auditing and analytical capabilities to matters of quality, we continue to execute a robust Quality Matters Process6 in support of our firm’s system of quality control to further drive audit quality accountability throughout our firm. Our assessment of the audit quality of our audit partners requires identified partner Audit Quality Events (AQEs), along with regional and office leadership accountability components, to be separately and distinctly evaluated as part of the annual performance management process. These evaluations are directly correlated to both a professional’s compensation considerations as well as his/her client engagement assignments.

For example, we rigorously examine all AQEs (both positive and negative) that occur during audits. Positive quality events often highlight an auditor’s independence, professional judgment, backbone, and accountability. Our auditors are steadfast in their commitment to reaching the correct accounting or auditing result regardless of client or internal pressure—even to the point of refusing to release an audit report if a client will not modify an improper accounting treatment that might be material to the financial statements.

Positive/Negative Quality Events

We have pre-established certain criteria for both for positive quality events and negative quality events—to assess these events when they arise in practice. Here are a few examples:

.png "Positive-Negative-Quality-Events-1-(2).png") Positive

Positive

-

Resolute determination was displayed to reach the correct accounting orauditing result regardless of client orinternal pressures.

-

Significant, active involvement in anengagement which demonstrated a focus on critical accounting and auditing areas and a tone with respect to audit quality.

-

Effective display of strong accounting and auditing knowledge and ability to support conclusions reached.

-

An inspection occurred and evidence of strong audit quality was present.

.png "Positive-Negative-Quality-Events-2-(1).png") Negative

Negative

-

Poor tone has been demonstrated with respect to a continued and biased support of a client’s improper accounting or disclosure position.

-

Substantial lack of involvement in an engagement was identified with regard to critical accounting and audit areas and/or poor tone with respect to audit quality.

-

Substantial lack of involvement on significant technical matters was identified during an audit.

-

An inspection occurred and a significant finding was made or restatement occurred.

Inspection Process

We gain significant insight from our internal and external inspection processes and use this knowledge to continuously adapt our firm-wide system of quality control.

Internal Inspections

Our internal inspection teams comprise partners, directors, and senior managers with appropriate technical knowledge, industry experience, and training to conduct a formal risk-based inspection of the firm’s assurance practice under the direction of the National Partner of Inspections.

A partner may be selected for inspection in any given year, and generally partners are subject to review at least once every three years. These reviews are conducted to:

-

Determine the quality of work performed

-

Confirm that our work complies with professional standards and firm policies and procedures

-

Monitor the effectiveness of remedial actions

The inspection team reviews, on a sample basis, the working papers and reports of each selected assurance engagement. The firm’s inspection program also includes a review of compliance with our quality control policies and procedures in other areas, including ethics, client acceptance and continuance, consultations, human resources, and other matters. These reviews involve focus group sessions with professional staff to help ensure the firm’s quality control procedures are properly understood.

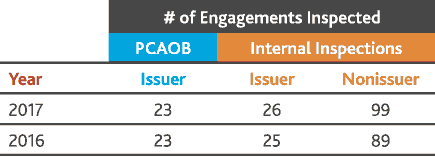

During 2017, we internally inspected 150 audit engagements—26 issuer clients, 99 non-issuer clients, and 25 employee benefit plan audits. This represents approximately 5.8% of the firm’s total assurance hours.

As a registered public accounting firm conducting over 300 issuer audit engagements, we must comply with annual inspection requirements of the PCAOB. The PCAOB’s inspection reports consist of two parts:

Part I: Public Portion

This section reports findings relating to specific audit engagements in which audit deficiencies may affect a firm’s ability to support its audit opinion. In addressing these findings, a firm takes appropriate corrective actions, including possible additional documentation or audit procedures (known as engagement remediation), and/or in rare cases revises its report. The inspection report and our response to the report can be found at: pcaobus.org/Inspections/Reports/Documents/104-2017-030-BDO.pdf.

Key findings in BDO’s 2015 report, the most current report available, align with findings across the profession and center primarily on testing of internal controls over financial reporting, management’s estimates, sampling, use of substantive analytical procedures and journal entries.

Part II: Non-Public Portion

This portion includes the PCAOB’s observations relating to a firm’s audit performance and quality controls where improvements are recommended. In evaluating a firm’s quality controls, the PCAOB assesses the following areas as part of that inspection:

-

Management structure and processes, including tone at the top

-

Practices for partner management, including allocation of partner resources and partner evaluation, compensation, admission, and disciplinary actions

-

Policies and procedures for considering and addressing the risks involved in accepting and retaining clients

-

Processes related to the firm’s use of audit work that the firm’s foreign affiliates perform on the foreign operations of the firm’s U.S. issuer audit clients

-

The firm’s processes for monitoring audit performance, including processes for identifying and assessing indicators of deficiencies in audit performance, independence policies and procedures, and processes for responding to weaknesses in quality control

Our most recent completed remediation activities that the PCAOB have assessed relate to the 2013 inspection of audits of 2012, for which the remediation period ended in October 2015. The PCAOB has accepted our remediation activities with respect to that period.

We consider the PCAOB inspection process along with our internal inspections to be valuable components of our firm’s overall approach to enhancing audit quality. Accordingly, we take inspection comments with the utmost seriousness, giving them prompt consideration. As outlined in this current and prior Audit Quality reports (2016, 2017) shared publicly, we have made, and continue to make, significant enhancements to our audit quality process, including investments in appropriate national resources, tools, training and communication, as well as in the design of specific action plans and monitoring of such plans. We are confident that these improvements are addressing all matters raised in the inspection reports. We expect our increased diligence and attention to audit quality on our current year-end audits will lead to further improvement in 2018.

Other Inspections

BDO is subject to periodic Quality Assurance Reviews (QARs) on behalf of BDO International. The objective of a QAR is to provide assurance that BDO member firms adhere to, and comply with, applicable professional standards, as well as BDO International’s standards. Such reviews are conducted on a rotating basis. We have received a draft of our report which reflects an acceptable level of performance in all functional areas.

As a member of the AICPA, we are subject to triennial external peer reviews of the portion of our auditing practice applicable to non-issuer engagements. Our most recent completed Peer Review was conducted in 2015 for which we received a “pass” rating. We are currently undergoing Peer Review to be concluded in the fall of 2018.

We view inspections as critically important to informing our overall audit process and take the process and the resulting findings extremely seriously. In comparing our firm findings, we find a strong correlation with overall profession findings by the PCAOB, AICPA and peer reviews. We monitor these trends closely. Our careful analysis as to the causes of issues revealed by these inspections help to pinpoint any problem areas we need to address on a firm-wide basis, such as enabling communications, enhancing tools or providing of additional guidance and education. Many of these enhancements have been previously described.

.png "Enginspected-(1).png")

Monitoring and Remediation

We vigilantly monitor and remediate any issues brought to light during an audit or during the inspection process. The areas where we have focused significant effort include:

-

Executing deep and specific risk assessment activities and linking them to effective controls and substantive responses

-

Demonstrating a deep and applied knowledge of ICFR

-

Performing a detailed audit focus on:

-

revenue-related topics

-

inventory

-

estimates

-

Operationally, we have gained insight from our cause analysis, monitoring and remediation, as well as from other inputs, including our National Assurance Survey, Quality Matters Process, Performance Management, and engagement team outreach. This insight has helped us to improve the timing of data collection and procedures to assess whether audit teams are applying tools and guidance in a timely way and to implement changes to learning programs in time to improve current year audit engagements.

SHARE