The State of Alliance Management

Alliances are becoming more and more a critical part of the fabric of corporate strategy across industries and functions, especially as peers in the life sciences, technology, and financial services industries find great success through their external relationships. Every few years, we survey our network to assess the state of alliance management: where we were, where we are, and where we are headed. The insights that follow in this piece are based on data gathered in 2021 and 2022 from 183 alliance and account management professionals across 11 industries, as well as more than 25 years’ worth of consulting for alliance management professionals to help them execute an increasingly diverse array of impactful and complex alliances.

We asked our respondents a few key questions to better understand the true state of alliance management today, and where it might be going next.

How Is the Use of Partnerships Evolving?

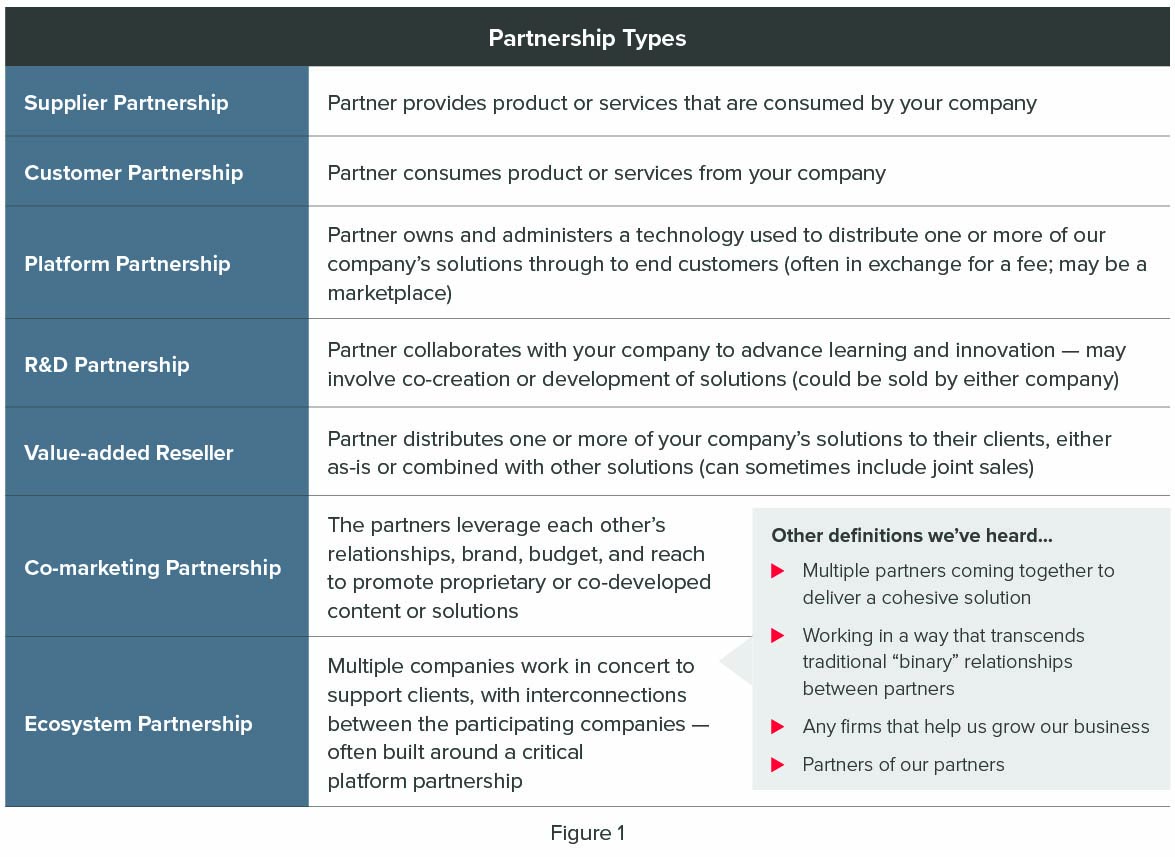

Companies are increasingly using a broad variety of alliance and partnership types (see Figure 1), and their investments are yielding returns. On average, alliances have driven one-third of company revenue during the past five years. Furthermore, our data suggest that performance is fairly consistent across alliance types — in other words, contribution to company performance depends on factors such as industry and alliance management maturity, not partnership type. Additionally, leaders and alliance professionals report that they expect the contribution of alliances to increase over the next five years. More than half (53 percent) of respondents further indicated that they expect significant growth to come from two to three different types of partnerships.

Alliances are not only seen as revenue drivers, but also as sources of innovation. Sixty-two percent of respondents reported that “Most” or “A great deal” of their innovation currently comes from collaborating with third parties.

Compared with five years ago, nearly twice as many respondents reported that “Most” of their innovation comes through collaboration with third parties. Over the next five years, it is expected that more than half of a company’s success will come from partnerships (either with competitors — coopetition — or with organizations that have no competitive overlap).

The study results are also fairly homogenous across the industries with the most representation in the data (life sciences, healthcare, financial services, and technology). Their share of total revenue from alliances over the last five years spans from 27 percent to 36 percent, with life sciences (which includes biopharma) being the lowest. Over the next five years, the four industries all expect a more than 70 percent increase in revenue from partnerships, with life sciences coming in highest at 84 percent.

But Are Alliances Delivering on Their Promise?

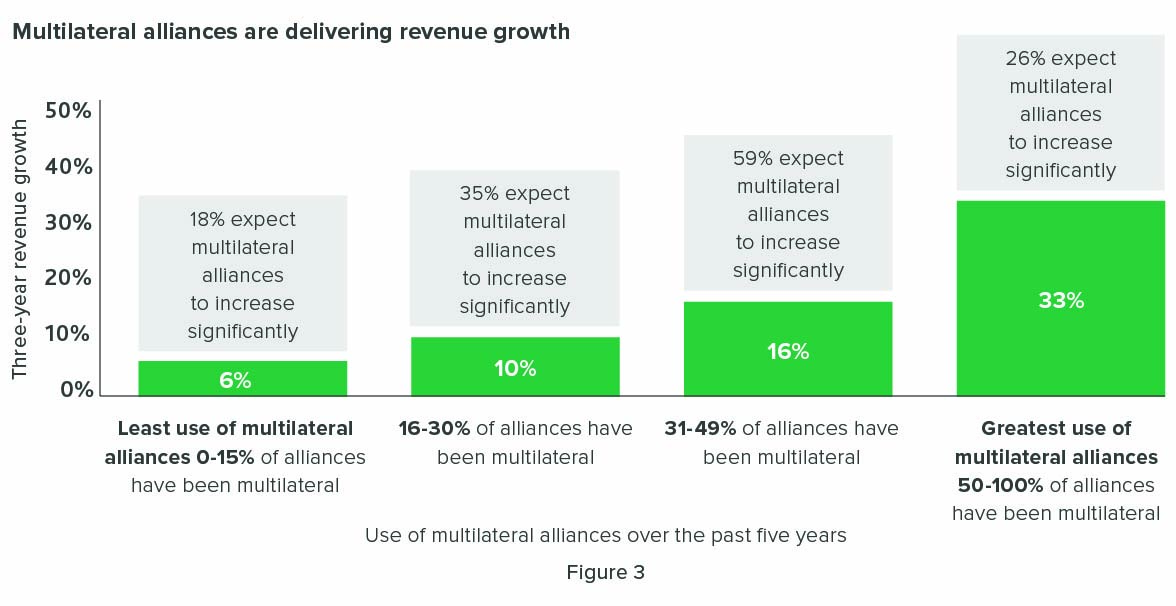

The results of our study are unambiguous: companies that rely more heavily on alliances have achieved significantly more revenue growth than those that rely least on alliances. Three-year revenue growth for companies with the greatest reliance on alliances was 27 percent, while growth for those with the lowest reliance on alliances was flat.

These results are consistent with findings from our 2020 study on coopetition. At companies expecting that more than 75 percent of future success would be the result of external assets and capabilities, revenue grew 73 percent more compared with companies that expect at least half of their success will come from internal assets and capabilities.

OK, but Don’t Many Alliances Fail?

Alliances are not a silver bullet, and success is not guaranteed.

Alliance failure rates from 1996 until today have remained relatively constant. Interestingly, we found that those companies that expect alliance revenue to increase over the next five years had a higher failure rate compared to those that thought alliance revenue would likely decrease. We suspect this reflects an openness to experimentation — and a greater comfort with failure — on the part of high-alliance-usage organizations. These companies are more likely to accept failure as part of the required investment in innovation. In the pharmaceutical industry in particular, many alliances fail for “technical” reasons, as the hypotheses about the effects of a compound or protein are invalidated by research.

When we control for organizational maturity in alliance management, failures are no more likely when they arise in the context of an alliance versus internal R&D, and the alliance has the benefit of spreading risk, cost, and learning across multiple organizations. Our study also found no correlation between alliance failure rates by industry and the revenue realized from alliances over the last five years.

Across different partnership types, we found that the highest failure rates occurred in platform and ecosystem partnerships, which is not surprising given the technical complexity associated with many of the former, and the commercial and collaboration challenges of the latter.

More than half of partnerships fail to fully achieve their objectives

What’s Contributing to Alliance Success or Failure?

Where should alliance professionals focus their efforts in order to optimize results? The top three reported contributors to alliance underperformance were:

1. Lack of internal alignment within at least one partner

2. Failure to understand differences in goals and priorities between partners

3. Lack of sufficiently robust joint governance Interestingly, the lowest reported contributor to alliance

failure was “Selected the wrong partner.” Human nature being what it is, blaming the partner when an alliance fails is often a natural reaction. While not terribly surprising, the fact that most alliance professionals do not fall prey to this tendency is a welcome finding — and yet another validation of the importance of having a professional alliance management function.

What Does It All Mean? Key Takeaways.

Alliances have become mainstream. Today, most organizations leverage alliances as a tool to drive customer value, deal with competitive threats, and enable innovation. The companies that realize the greatest returns on their alliances share several characteristics. They:

- Use multiple alliance models, including multilateral alliances

- Expect that some alliances will fail to deliver on their potential

- Cull lessons from every alliance — successful or unsuccessful — to inform future choices

- Invest heavily in mechanisms to spot and address gaps in alignment within their company, as well as between them and their alliance partners

Across industries, more companies today are building robust, mature alliance management capabilities (see Figure 6),

and these are the companies that our research indicates will deliver the best results for their customers, employees, and shareholders over the next few years.

SHARE