The Medical Care Consumer Price Index (CPI), issued by the U.S. Bureau of Labor Statistics, measures inflation by tracking retail prices of a good or service of a constant quality and quantity over time. It is frequently used by providers and insurers for their financial forecasts and benchmarking, as well as policymakers to understand and respond to healthcare trends.

Despite its widespread use, the Medical Care CPI is not an accurate representation of rising healthcare costs for most consumers nor companies. The CPI’s basket of goods and services does not reflect cost changes most relevant to these populations and excludes major drivers of premium growth, such as high-cost specialty drugs and shifting utilization patterns. If payers and providers continue to anchor expectations to outdated or misaligned inflation benchmarks, they risk underestimating financial pressures and miscommunicating key trends.

Tracking the Medical Care CPI

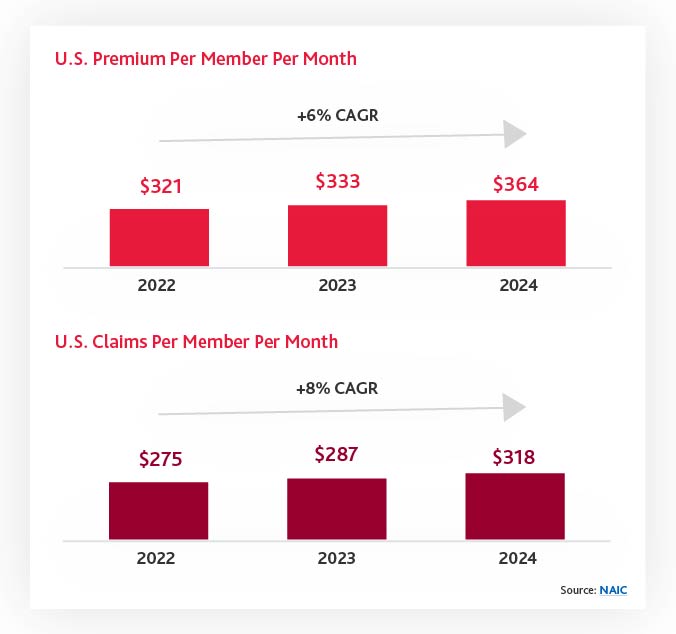

To understand the issues with the Medical Care CPI, it helps to first look at two other healthcare metrics: health insurance premiums Per Member Per Month (PMPM) and claims PMPM. Premiums PMPM have increased at a rate of 6% Compound Annual Growth Rate (CAGR) over the past three years while claims have increased by 8%. This gap illustrates fundamental challenges where premium increases are not keeping up with claims expenses, making the forecasts created with the Medical Care CPI inaccurate compared to actual spend.

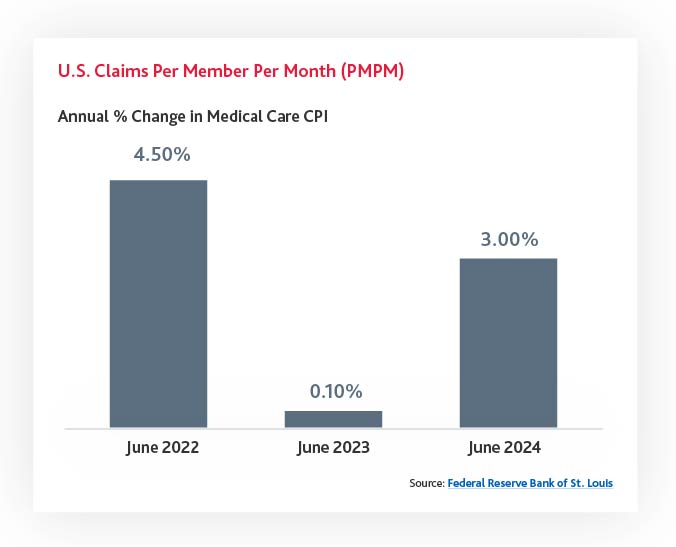

Furthermore, both premium PMPM and claims PMPM are significantly higher than the Medical Care CPI, which was only 3.0% in June 2024 from the previous year, 0.1% in 2023, and 4.5% in 2022. These numbers fall significantly below recorded premium and claims expenses.

Understanding the Root Causes of the Disconnect

There are several systemic issues that explain why the Medical Care CPI diverges from the true cost trajectory of health insurance:

Broaden Benchmarking Metrics

Supplement the CPI with other indices and metrics, such as the NAIC premium expense index, specialty drug trend reports, and utilization/mix trend analyses.

Track Specialty Drug Impact

Build forecasting and strategy tools that incorporate the rising influence of specialty pharmaceuticals on total cost of care.

Analyze Internal Data

Leverage your organization’s own claims, utilization, and cost data to understand localized or plan-specific trends that the CPI cannot reflect.

Educate Stakeholders

Help internal teams, regulators, and members understand why premiums are rising faster than the CPI would suggest, resetting expectations and fostering transparency.

Accept and Plan for Reality

Acknowledge that this disconnect isn’t going away, and work with your teams to build financial models and communication strategies accordingly.