FASB Updates Segment Reporting Disclosures

BY ACCESSING THE FASB DOCUMENTS ON THIS SITE, YOU ACCEPT AND AGREE TO THESE FASB TERMS AND THE WEBSITE TERMS AS APPLIED TO YOUR USE OF THIS SITE OR ANY FASB LICENSED DOCUMENTS

This Bulletin was updated for comments from the SEC staff at 2023 AICPA & CIMA Conference on Current SEC and PCAOB Developments.

Summary

The FASB recently updated U.S. GAAP to require additional disclosures by public entities about certain expenses. More specifically, all public entities will begin disclosing new segment expense information in response to investor requests for additional details. The new requirements will result in incremental disclosures in annual and interim reports. They apply to fiscal years beginning after December 15, 2023, and interim periods within fiscal years beginning after December 15, 2024. The new guidance must be applied retrospectively to all prior periods presented in the financial statements unless impracticable. Early adoption is permitted.

Main Provisions

Accounting Standards Update 2023-07 (the “ASU”) requires all public entities, including those with a single reportable segment, to disclose “significant segment expenses” and “other segment items” for each reportable segment. There is no requirement to reconcile the new information to the corresponding consolidated expense financial statement captions. In addition, all of the existing annual disclosures about a reportable segment’s profit or loss and assets will now be provided in interim periods too. See the appendix for an example.

The ASU also permits (but does not require) entities to disclose multiple measures of a segment’s profit or loss if the chief operating decision maker (the “CODM”) uses these measures to allocate resources and assess segment performance. However, at least one of the disclosed measures must be the measure most consistent with U.S. GAAP measurement principles. Entities must reconcile each measure of segment profit or loss to the consolidated income statement annually and on an interim basis. There are no other reconciliation requirements for interim financial statements.

Additional Measures of Segment Profit or Loss

As discussed above, the ASU permits, but does not require additional measures of segment profit or loss within the financial statements. The ASU does not require these additional measures to be consistent with the recognition and measurement principles of U.S. GAAP, which may otherwise result in the disclosure of multiple measures of segment performance that are considered to be “non-GAAP” financial measures.

At the 2023 AICPA & CIMA Conference on Current SEC and PCAOB Developments (the “Conference”), the SEC staff expressed its view that additional measures of segment performance that are not calculated in accordance with U.S. GAAP are not “expressly permitted.” As a result, such measures are subject to the SEC’s rules on non-GAAP measures, which technically prohibit the inclusion of additional non-GAAP measures of segment performance in the financial statements.

Entities that wish to early adopt the provisions of the ASU should contact the SEC staff in advance of filing if they plan to disclose additional non-GAAP measures of segment performance. The SEC staff offered the following considerations for such entities:

- At a minimum, entities must continue to disclose the measure of segment profit or loss that is most consistent with U.S. GAAP.

- Any measures of segment performance disclosed by entities should be regularly reviewed by the CODM and used by the CODM to allocate resources and assess performance.

- Any additional measures of segment performance that are a non-GAAP financial measure must not be misleading and must:

- Comply with Regulation G and Item 10(e) of Regulation S-K

- Include a statement disclosing why the non-GAAP measures are useful to investors

- Include the required reconciliations to the nearest U.S. GAAP measure

The directive for entities to call the SEC staff in advance of adopting the ASU and disclosing additional measures of non-GAAP segment performance is not a long-term solution. We anticipate that the SEC staff will issue further guidance with its views on this topic in the coming months prior to the ASU’s effective date.

Significant Segment Expenses

The new guidance introduces the significant expense principle, which requires public entities to disclose expenses for each reportable segment that meet all of the following criteria:

- Regularly provided to the CODM

- Included in reported segment profit or loss

- Determined to be significant based on qualitative and quantitative factors

The principle applies to allocated corporate overhead expenses and each reported measure of a segment’s profit or loss. Entities with financial operations segments that disclose net interest expense must disclose gross interest expense, if interest expense meets the significant expense principle criteria.

The ASU also introduces the concept of easily computable information. That is, the CODM may be regularly provided with expense information in alternative forms including ratios or percentages. For example, the CODM may be provided with segment revenue and segment gross margin. Cost of sales is easily computable from this information and therefore, entities must disclose cost of sales if considered significant. Entities should focus on the substance of the information regularly provided to the CODM rather than its form.

Other Segment Items

The ASU requires entities to disclose an amount and qualitative description of other segment items for each reportable segment. These items represent the difference between a segment’s profit or loss and segment revenues less significant segment expenses.

The new guidance requires disclosing other significant items, regardless of whether significant segment expenses are disclosed. Entities that do not disclose significant segment expenses must disclose the expense information used by the CODM to manage operations. For example, entities may disclose that the CODM is regularly provided with only budgeted or forecasted expense information for a reportable segment or that the CODM uses consolidated expense information.

Other Disclosures

In addition to the significant segment expense information and other segment items, the ASU requires entities to disclose the following:

- Title and position of the CODM

- Explanation of how the CODM uses the reported measure(s) of segment profit or loss in assessing segment performance and deciding how to allocate resources

- Significant changes from prior periods in expense measurement and allocation methods and their effect, if any, on the measure of segment profit or loss

- Changes in the method for allocating centrally incurred expenses and their effect, if any, on the measure of segment profit or loss

Single Reportable Segment Entities

Entities with a single reportable segment must disclose all of the existing disclosures required by ASC 280, as well as the measure of profit or loss used by the CODM to allocate resources and assess performance that is most consistent with U.S. GAAP.

The ASU highlights that such entities may distinguish the business activities of the single operating segment from those of the consolidated entity. For example, certain functional departments or corporate headquarters may not be part of the single operating segment. In those situations, the CODM may regularly review the operating results and performance of the single operating segment differently than how management assesses the consolidated entity’s performance. Alternatively, if the single operating segment represents the entire consolidated entity, the CODM may regularly review the entity-wide operating results and performance.

At the Conference, the SEC staff stated that it expects the measure of segment performance for an entity with a single reportable segment that is managed on a consolidated basis to be consolidated net income.

Duplicating Information from the Primary Financial Statements

When the CODM of a single operating segment entity uses a consolidated profit or loss measure presented on the entity's income statement, the disclosures required by the significant expense principle and existing segment requirements may result in duplicative information in the segment footnote. In such cases, an entity may choose to reference the primary financial statements in the segment footnote. While duplication is not prohibited, the FASB believes that duplicating the entire consolidated income statement in the segment footnote is unnecessary.

Recasting of Prior Period Segment Information

As amended by the ASU, ASC 280 requires entities to recast prior period segment information, including significant segment expenses, in the following situations unless it is impracticable to do so:

- When the composition of reportable segments changes

- When significant segment expense categories change due to changes in the segment information regularly provided to the CODM

If recasting prior period significant segment expenses is impracticable, entities must disclose both the new and old significant segment expense categories.

If significant segment expense categories and amounts change due to changes in measurement methods, entities are not required to recast prior period significant segment expenses, but it is preferable to do so.

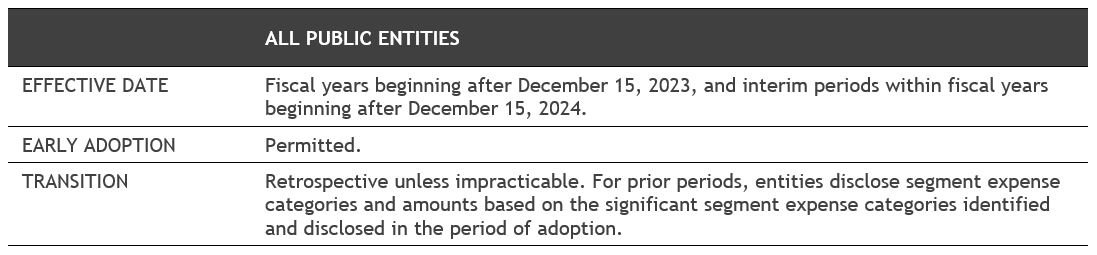

Effective Dates and Transition

The following table summarizes transition for the ASU:

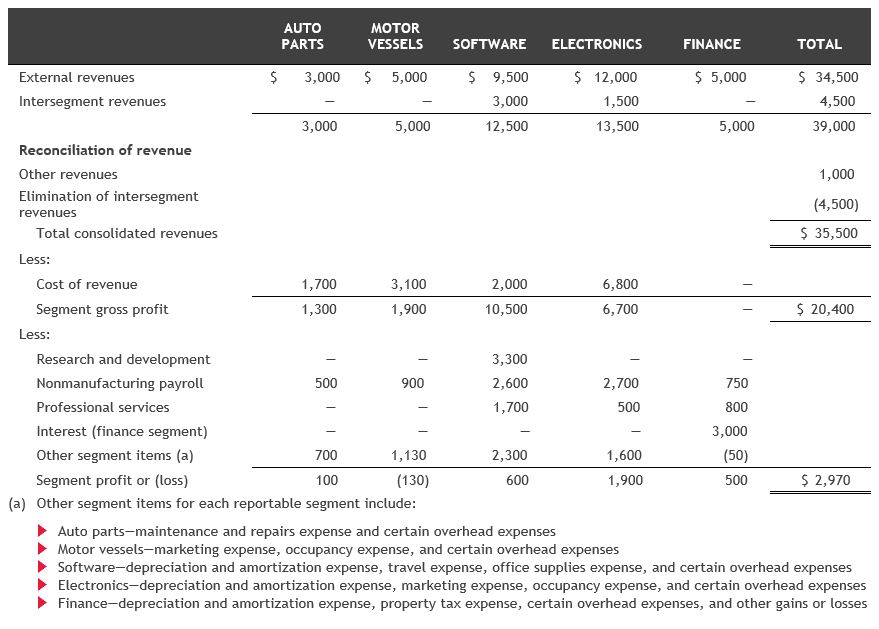

Appendix: Example Disclosure

The following example has been adapted from the ASU1 to illustrate how entities can report significant segment expenses and other segment items. This table omits a reconciliation of segment profit and loss to the entity’s consolidated totals for simplicity.

1 See ASC 280-10-55-48

SHARE