ISSB Global Adoption and Considerations for Multinational Companies

Mandatory reporting aligned with the ISSB Standards continues to advance across a growing number of jurisdictions, reinforcing the ISSB’s role as the global baseline for investor-focused sustainability disclosures. While some companies are now legally required to report under ISSB-aligned rules, many others are evaluating voluntary adoption, driven by participation in global capital markets and the convergence of legacy sustainability reporting standards and frameworks. Details on global implementation of the ISSB Standards, as well as considerations for voluntary use, are below.

About the ISSB Standards

The IFRS Sustainability Disclosure Standards, often referred to as the ISSB Standards, help companies provide sustainability-related information that is material to investors across global markets (i.e., a global baseline). The standards are developed by the International Sustainability Standards Board (ISSB), an independent board that is part of the International Financial Reporting Standards (IFRS) Foundation, and are compatible with the IFRS Accounting Standards.

Currently, the ISSB Standards consist of IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures. The standards build upon widely used, pre-existing approaches to sustainability reporting – including the industry-specific SASB Standards and the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD). The ISSB now maintains the SASB Standards (updates are underway), and the task force that developed and maintained the TCFD framework has disbanded and transferred monitoring activities to the IFRS Foundation.

In addition, the ISSB is in the early stages of developing a new resource for nature-related disclosures, which will draw from the recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD) and complement IFRS S1 and IFRS S2.

Mandatory Global ISSB Application

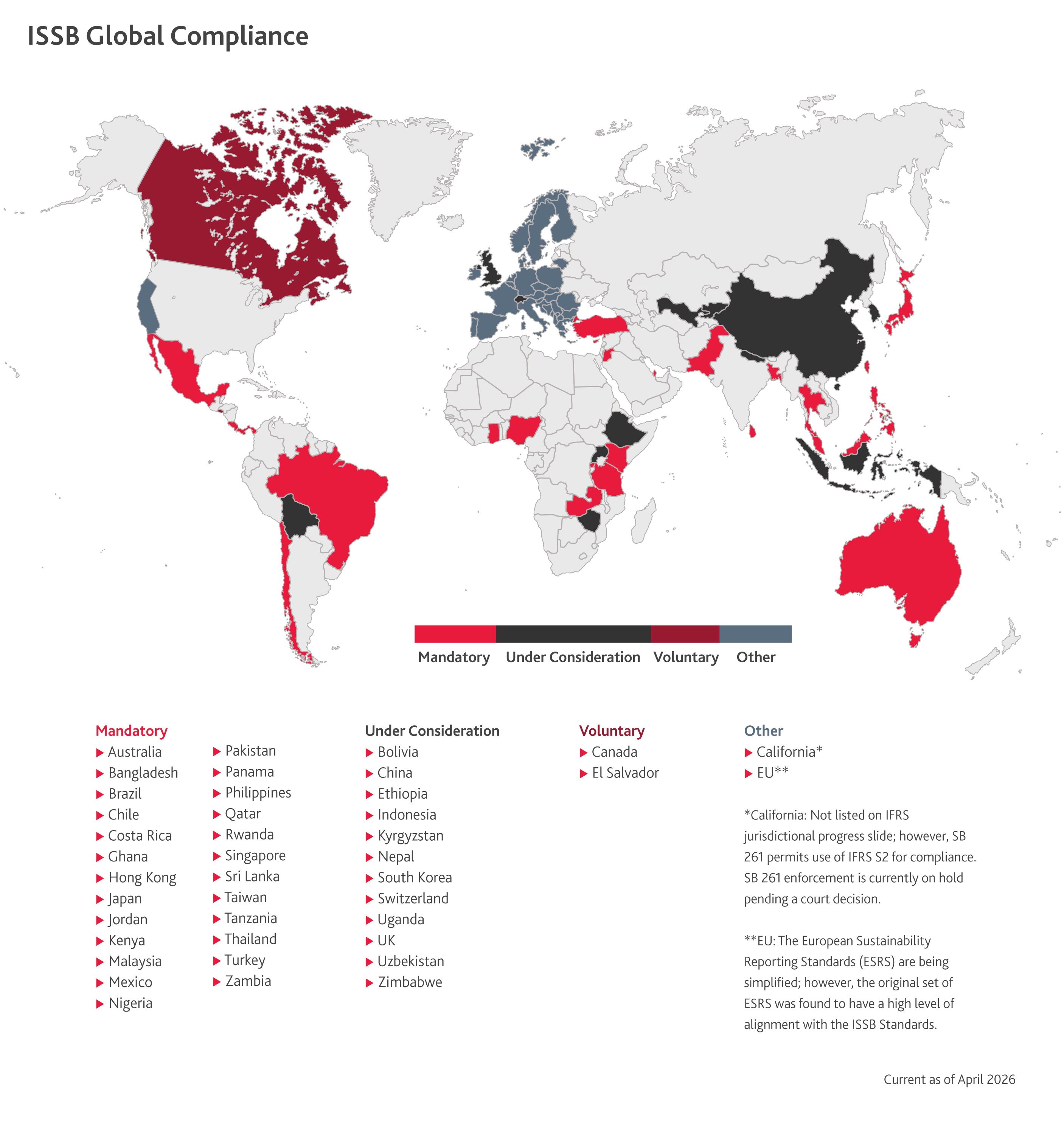

Companies may be subject to mandatory reporting requirements in jurisdictions that have legally adopted the standards. Adoption takes different forms — some jurisdictions develop local standards based on the ISSB Standards or incorporate them into existing requirements, whereas others reference IFRS S1 and/or IFRS S2 directly (sometimes with additional transitional relief to support initial compliance).

According to IFRS materials published in March 2026, 40 jurisdictions have decided to use or are taking steps to introduce ISSB Standards into their legal frameworks, representing approximately 60% of global GDP.

A BDO analysis of global ISSB compliance revealed the following:

- Mandatory ISSB compliance has been adopted in 25 jurisdictions, concentrated in Asia and Africa (~40% and 25%, respectively).

- In most of these jurisdictions, reporting periods have already begun to phase in.

- Compliance is often limited to public companies and/or financial institutions, but some requirements also apply to other types of entities (e.g., large non-listed companies).

- While some mandates are limited to climate reporting, about 80% of jurisdictions require broader sustainability disclosures once requirements are fully implemented.

- Local reporting mandates often apply to both foreign and domestic entities that meet scoping requirements. The adoption of ISSB Standards varies across jurisdictions in terms of how rules are applied to foreign entities, whether reports using equivalent standards are accepted, and whether domestic subsidiaries may rely on foreign parent consolidated reporting for relief from separate reporting.

Entities that believe they may be subject to mandatory reporting requirements should consult their legal counsel.

Voluntary Application: A Multinational Perspective

Because ISSB is designed to support decision-useful communication with global investors, lenders, and other capital providers, multinational and large publicly traded companies may find value in ISSB-aligned reporting — even if they aren’t subject to regulatory requirements that mandate these disclosures.

The ISSB has published guidance for voluntary application of the ISSB Standards, which includes taking a phased approach while building up reporting capacity while transparently disclosing incomplete compliance. Although the ISSB Standards do not require assurance over reporting (these requirements may be established by individual jurisdictions as they formally adopt the standards), the guidance identifies third-party assurance as a way to help build user confidence when standards are only partially applied.

In the U.S., many companies already use SASB and TCFD in their sustainability reporting, both of which have been integrated into the ISSB Standards. This creates a strong foundation for companies to transition to ISSB reporting if they choose to do so. To support this process, the ISSB has published educational materials that outline how leveraging SASB and TCFD disclosures can help companies move toward ISSB Standards compliance. Additionally, some U.S. multinationals may find that their global subsidiaries are subject to mandatory ISSB disclosures and choose to align group-wide reporting to avoid fragmentation.

Contact BDO for help building a sustainability reporting strategy that’s right for your company.