Global Tax Reform

Changing the Global Taxation Playing Field

Global tax reform is on a crescendo. Policymakers across countries are addressing the globalization of business activity by working toward a fairer tax system - a global tax framework. With reform comes ongoing change and considerable implications for multinational businesses.

BDO keeps a close watch on global tax reform and shares what it means to global organizations.

Key Takeaways

1.

Global tax reform continues to take shape after years of negotiations. The digitalization and globalization of businesses led to a developing global tax framework that stands on two key underpinnings: Pillar One and Pillar Two.

2.

Change is coming –The Organisation for Economic Cooperation and Development (OECD) is aiming for implementation of its two-pillar global tax framework in 2023-2024. So far, 137 countries are in agreement with the framework’s provisions since it was rolled out in 2021.

3.

With the release of the OECD’s agreed-upon framework, negotiations began on the model rules for Pillars One and Two. Model rules for Pillar Two were issued. Meanwhile, the OECD requested stakeholder comments on draft Pillar One rules. Due to the inherent complexity of the proposals, the OECD delayed implementation of Pillar One.

4.

U.S.-based multinational enterprises (MNEs) should monitor developments and review the final rules to assess any potential impact to their businesses. They should also keep track of implementation progress in all countries in which they operate.

5.

BDO has broad and deep expertise in helping multinational organizations navigate global tax reform opportunities and challenges. Our Transfer Pricing and International Tax practices can help you evaluate the potential impact of Pillars One and Two on your business.

Five Key Areas to Explore

![]()

Background

![]()

Two-Pillar Framework

![]()

Preparation

![]()

BDO's Take

![]()

Insights

Background

The OECD will develop implementation guidance for OECD/G20 Inclusive Framework on BEPS (IF) countries. The IF is a network of countries collaborating on ways to address base erosion and profit shifting (BEPS) issues. The Pillar One proposal calls for implementation through a multilateral instrument that would be developed and signed by IF countries in 2023, for implementation in 2024.

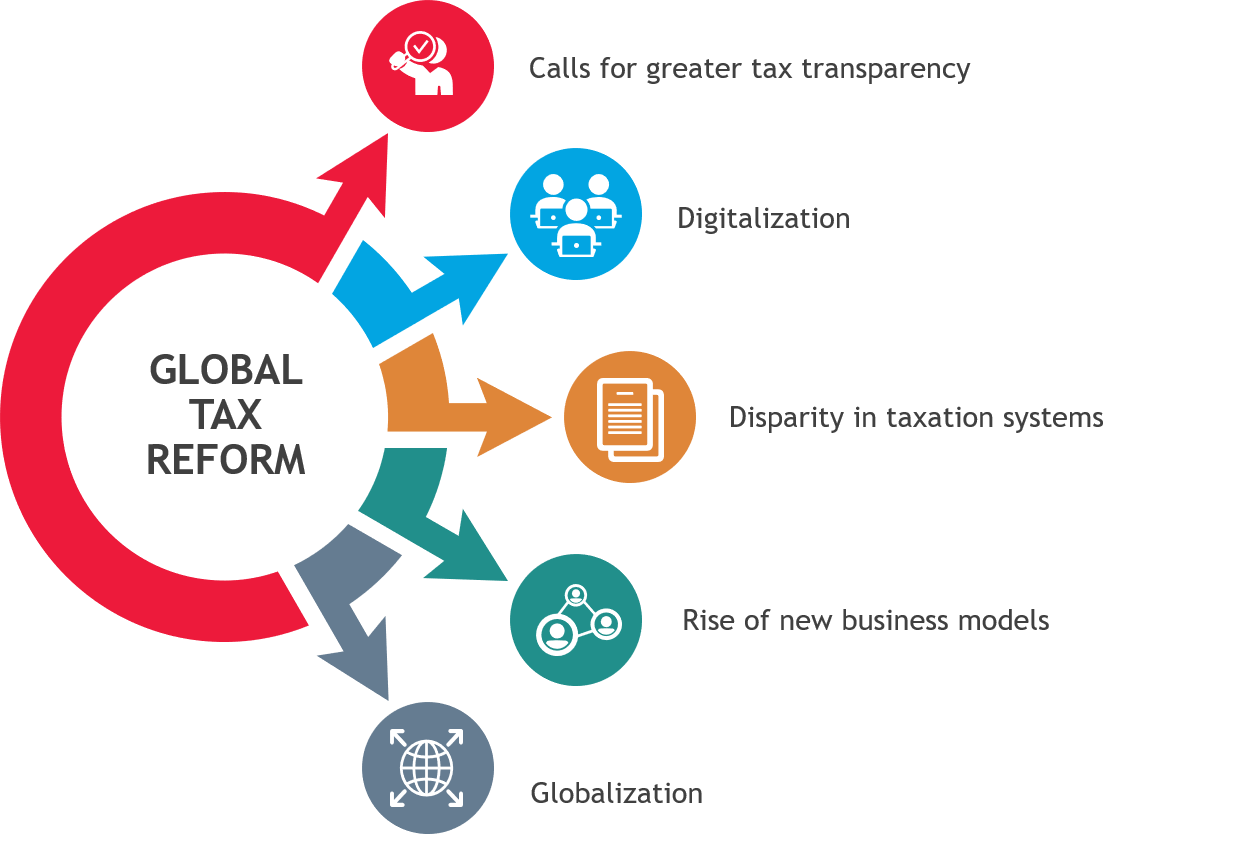

Top Drivers of Global Tax Reform

Two-Pillar Framework

Pillar One | Pillar Two | |

|---|---|---|

| Summary | This changes some nexus and profit allocation rules for taxation. The signatories to the IF statement committed to provide the necessary coordination between the new rules and the removal of all digital service taxes. | This attempts to stop the “race to the bottom” by jurisdictions lowering their corporate income tax rates. Pillar Two establishes a global corporate minimum tax rate of 15%. |

| In-scope MNEs | Threshold: Global revenue above EUR 20 billion and profitability above 10%. That threshold could be reduced to EUR 10 billion upon review seven years after the agreement enters into force. | Threshold: Global revenue above EUR 750 million. |

| Out-of-scope Industries |

|

|

Preparation

U.S. MNEs that are in scope for either pillar of the framework may see an increase in the complexity of their tax profiles and potentially an increase in their total tax liability.

Companies should scenario plan to determine the outcomes for the parts of their businesses that are subject to Pillar One and/or Pillar Two and how those outcomes may require changes in their tax strategies. They should also determine whether they need to reevaluate their business and operating models to better align with global tax policies.

BDO's Take

The legislative bodies of the 130+ countries that have signed the agreement will need to take action to enact the new rules into domestic law. Work on the implementation into domestic law is well underway in many jurisdictions, including all EU member states, with most adhering to a planned entry into force in 2024. It is important to continue to monitor global developments to determine which jurisdictions will keep to this timetable.

Insights

The latest updates and historical perspectives around the globe.

2023

AUG 2023 | OECD ISSUES PILLAR TWO ADMINISTRATIVE GUIDANCE, INFORMATION RETURN, AND STTR GUIDANCE

JULY 2023 | PILLAR 2: TIME FOR US MULTINATIONAL ENTERPRISES TO ACT

JUNE 2023 | BEPS 2.0: ADDRESSING THE IMPACT OF GLOBAL TAX REFORM

MAY 2023 | TAX TECHNOLOGY ON THE GLOBAL STAGE - TAX AT THE SPEED OF TECH PODCAST SERIES

SEPT 2022 | FOUR REASONS TO ALIGN YOUR SUPPLY CHAIN AND TAX STRATEGIES

SEPT 2022 | OECD HOLDS PUBLIC CONSULTATION ON PILLAR ONE PROGRESS REPORT

AUG 2022 | U.S. BOOK MINIMUM TAX AFFECTS SOME NON-U.S. MULTINATIONALS

AUG 2022 | COMMENTS ON PROGRESS REPORT ON AMOUNT A OF PILLAR ONE

APRIL 2022 | OECD’S PILLAR TWO RULES COULD HAVE LASTING IMPACT ON MULTINATIONAL GROUPS

MARCH 2022 | BDO SUBMISSION TO THE OECD ON THE PUBLIC CONSULTATION DOCUMENT

FEB 2022 | OECD ISSUES DRAFT RULES FOR TAX BASE DETERMINATIONS UNDER AMOUNT A OF PILLAR ONE

DEC 2021 | EU PROPOSED DIRECTIVE FOR PILLAR TWO

NOV 2021 | GLOBAL TAX: OECD ANNOUNCEMENT OF AGREEMENT ON INTERNATIONAL TAX REFORM

OCT 2021 | OECD ANNOUNCES AGREEMENT ON GLOBAL TAX REFORM

OCT 2021 | REGIONAL PERSPECTIVES ON GLOBAL TAX REFORM

AUG 2021 | GLOBAL TAX REFORM: WHAT CAN TAXPAYERS DO TO PREPARE FOR THE CHANGES?

JUNE 2021 | G-20 BACKS G-7 SUPPORT FOR GLOBAL MINIMUM TAX AND NEW ALLOCATION RULES

JUNE 2021 | G-7 FINANCE MINISTERS ANNOUNCE SUPPORT FOR GLOBAL MINIMUM TAX AND NEW ALLOCATION RULES

Webcast

The Intersection of Tax & ESG Webcast Series: Sustainable Value Creation for Multinational Companies

October 10, 2023

Webcast

Practical Advice for Managing Pillar Two - Global Minimum Tax

July 25, 2023

Webcast

2023 Tax Strategist Cross-Borders: Spring Planning Session

May 3, 2023

Webcast

BDO Tax Strategist: Cross-Border Issues – Year-End Considerations

December 14, 2022

Webcast

OECD Pillar II - Global Anti-Base Erosion (GloBE): How Multinational Enterprises (MNEs) Can Prepare

September 20, 2022